Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSequential Estimation of Nonparametric Correlation using Hermite Series Estimators

Dec 11, 2020

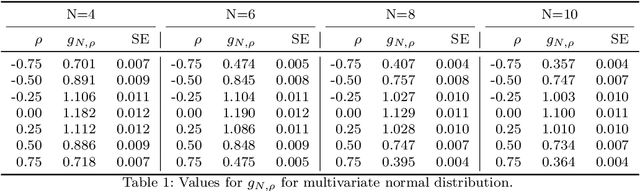

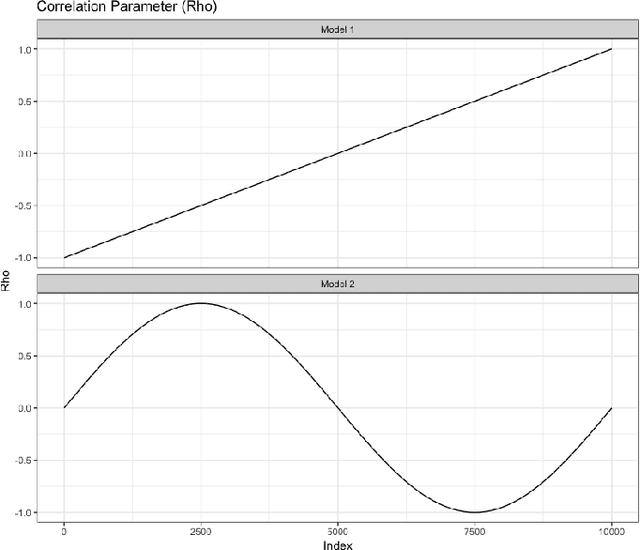

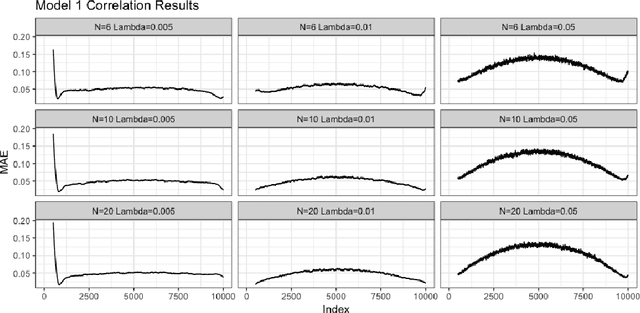

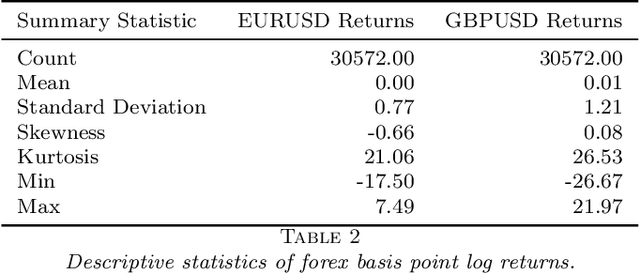

In this article we describe a new Hermite series based sequential estimator for the Spearman's rank correlation coefficient and provide algorithms applicable in both the stationary and non-stationary settings. To treat the non-stationary setting, we introduce a novel, exponentially weighted estimator for the Spearman's rank correlation, which allows the local nonparametric correlation of a bivariate data stream to be tracked. To the best of our knowledge this is the first algorithm to be proposed for estimating a time-varying Spearman's rank correlation that does not rely on a moving window approach. We explore the practical effectiveness of the Hermite series based estimators through real data and simulation studies demonstrating good practical performance. The simulation studies in particular reveal competitive performance compared to an existing algorithm. The potential applications of this work are manifold. The Hermite series based Spearman's rank correlation estimator can be applied to fast and robust online calculation of correlation which may vary over time. Possible machine learning applications include, amongst others, fast feature selection and hierarchical clustering on massive data sets.

Sequential Quantiles via Hermite Series Density Estimation

Mar 04, 2017

Sequential quantile estimation refers to incorporating observations into quantile estimates in an incremental fashion thus furnishing an online estimate of one or more quantiles at any given point in time. Sequential quantile estimation is also known as online quantile estimation. This area is relevant to the analysis of data streams and to the one-pass analysis of massive data sets. Applications include network traffic and latency analysis, real time fraud detection and high frequency trading. We introduce new techniques for online quantile estimation based on Hermite series estimators in the settings of static quantile estimation and dynamic quantile estimation. In the static quantile estimation setting we apply the existing Gauss-Hermite expansion in a novel manner. In particular, we exploit the fact that Gauss-Hermite coefficients can be updated in a sequential manner. To treat dynamic quantile estimation we introduce a novel expansion with an exponentially weighted estimator for the Gauss-Hermite coefficients which we term the Exponentially Weighted Gauss-Hermite (EWGH) expansion. These algorithms go beyond existing sequential quantile estimation algorithms in that they allow arbitrary quantiles (as opposed to pre-specified quantiles) to be estimated at any point in time. In doing so we provide a solution to online distribution function and online quantile function estimation on data streams. In particular we derive an analytical expression for the CDF and prove consistency results for the CDF under certain conditions. In addition we analyse the associated quantile estimator. Simulation studies and tests on real data reveal the Gauss-Hermite based algorithms to be competitive with a leading existing algorithm.

* 43 pages, 9 figures. Improved version incorporating referee comments, as appears in Electronic Journal of Statistics