Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLearning Individual Behavior in Agent-Based Models with Graph Diffusion Networks

May 27, 2025

Agent-Based Models (ABMs) are powerful tools for studying emergent properties in complex systems. In ABMs, agent behaviors are governed by local interactions and stochastic rules. However, these rules are, in general, non-differentiable, limiting the use of gradient-based methods for optimization, and thus integration with real-world data. We propose a novel framework to learn a differentiable surrogate of any ABM by observing its generated data. Our method combines diffusion models to capture behavioral stochasticity and graph neural networks to model agent interactions. Distinct from prior surrogate approaches, our method introduces a fundamental shift: rather than approximating system-level outputs, it models individual agent behavior directly, preserving the decentralized, bottom-up dynamics that define ABMs. We validate our approach on two ABMs (Schelling's segregation model and a Predator-Prey ecosystem) showing that it replicates individual-level patterns and accurately forecasts emergent dynamics beyond training. Our results demonstrate the potential of combining diffusion models and graph learning for data-driven ABM simulation.

Can Generative AI agents behave like humans? Evidence from laboratory market experiments

May 12, 2025We explore the potential of Large Language Models (LLMs) to replicate human behavior in economic market experiments. Compared to previous studies, we focus on dynamic feedback between LLM agents: the decisions of each LLM impact the market price at the current step, and so affect the decisions of the other LLMs at the next step. We compare LLM behavior to market dynamics observed in laboratory settings and assess their alignment with human participants' behavior. Our findings indicate that LLMs do not adhere strictly to rational expectations, displaying instead bounded rationality, similarly to human participants. Providing a minimal context window i.e. memory of three previous time steps, combined with a high variability setting capturing response heterogeneity, allows LLMs to replicate broad trends seen in human experiments, such as the distinction between positive and negative feedback markets. However, differences remain at a granular level--LLMs exhibit less heterogeneity in behavior than humans. These results suggest that LLMs hold promise as tools for simulating realistic human behavior in economic contexts, though further research is needed to refine their accuracy and increase behavioral diversity.

On learning agent-based models from data

May 10, 2022

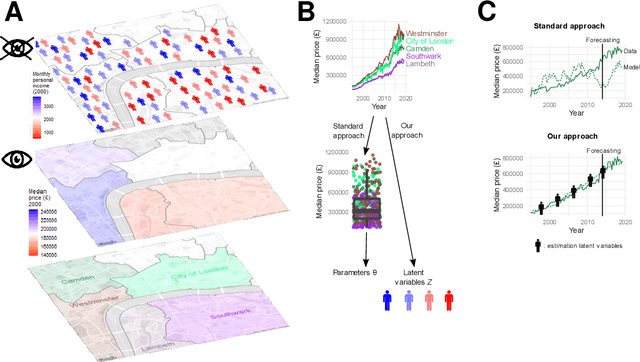

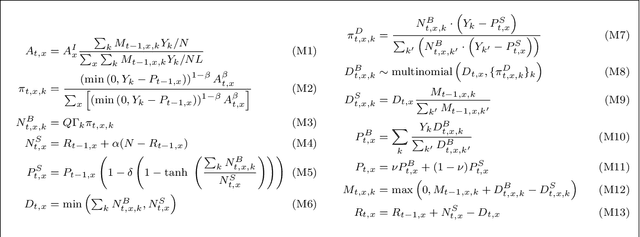

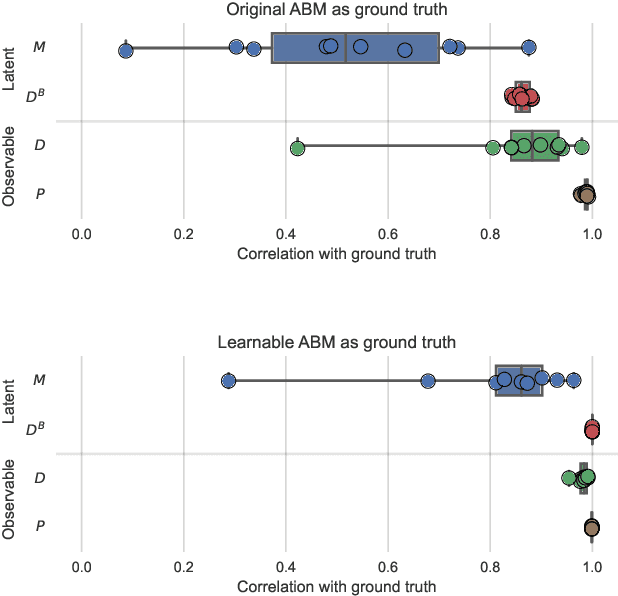

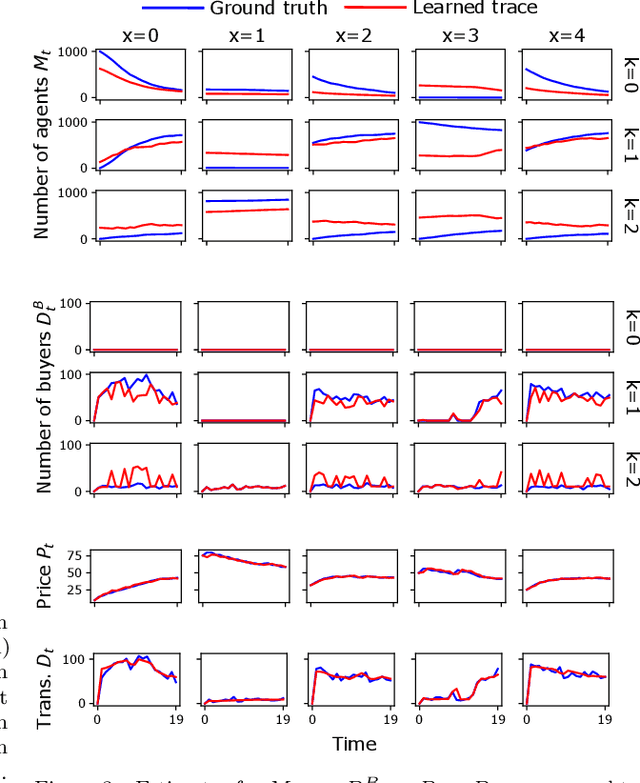

Agent-Based Models (ABMs) are used in several fields to study the evolution of complex systems from micro-level assumptions. However, ABMs typically can not estimate agent-specific (or "micro") variables: this is a major limitation which prevents ABMs from harnessing micro-level data availability and which greatly limits their predictive power. In this paper, we propose a protocol to learn the latent micro-variables of an ABM from data. The first step of our protocol is to reduce an ABM to a probabilistic model, characterized by a computationally tractable likelihood. This reduction follows two general design principles: balance of stochasticity and data availability, and replacement of unobservable discrete choices with differentiable approximations. Then, our protocol proceeds by maximizing the likelihood of the latent variables via a gradient-based expectation maximization algorithm. We demonstrate our protocol by applying it to an ABM of the housing market, in which agents with different incomes bid higher prices to live in high-income neighborhoods. We demonstrate that the obtained model allows accurate estimates of the latent variables, while preserving the general behavior of the ABM. We also show that our estimates can be used for out-of-sample forecasting. Our protocol can be seen as an alternative to black-box data assimilation methods, that forces the modeler to lay bare the assumptions of the model, to think about the inferential process, and to spot potential identification problems.