Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeBackground Knowledge Injection for Interpretable Sequence Classification

Jun 25, 2020

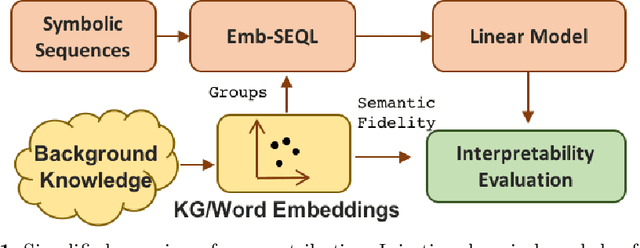

Sequence classification is the supervised learning task of building models that predict class labels of unseen sequences of symbols. Although accuracy is paramount, in certain scenarios interpretability is a must. Unfortunately, such trade-off is often hard to achieve since we lack human-independent interpretability metrics. We introduce a novel sequence learning algorithm, that combines (i) linear classifiers - which are known to strike a good balance between predictive power and interpretability, and (ii) background knowledge embeddings. We extend the classic subsequence feature space with groups of symbols which are generated by background knowledge injected via word or graph embeddings, and use this new feature space to learn a linear classifier. We also present a new measure to evaluate the interpretability of a set of symbolic features based on the symbol embeddings. Experiments on human activity recognition from wearables and amino acid sequence classification show that our classification approach preserves predictive power, while delivering more interpretable models.

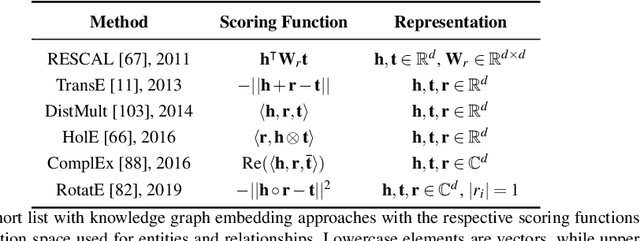

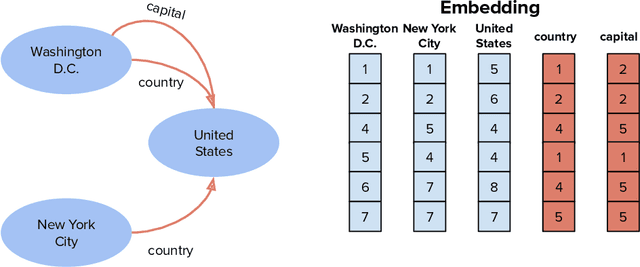

Knowledge Graph Embeddings and Explainable AI

Apr 30, 2020

Knowledge graph embeddings are now a widely adopted approach to knowledge representation in which entities and relationships are embedded in vector spaces. In this chapter, we introduce the reader to the concept of knowledge graph embeddings by explaining what they are, how they can be generated and how they can be evaluated. We summarize the state-of-the-art in this field by describing the approaches that have been introduced to represent knowledge in the vector space. In relation to knowledge representation, we consider the problem of explainability, and discuss models and methods for explaining predictions obtained via knowledge graph embeddings.

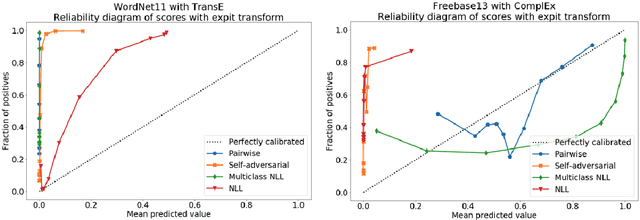

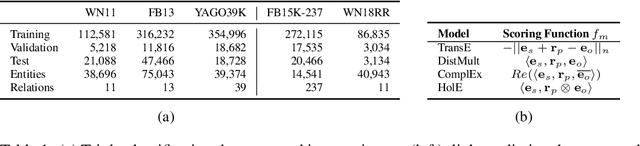

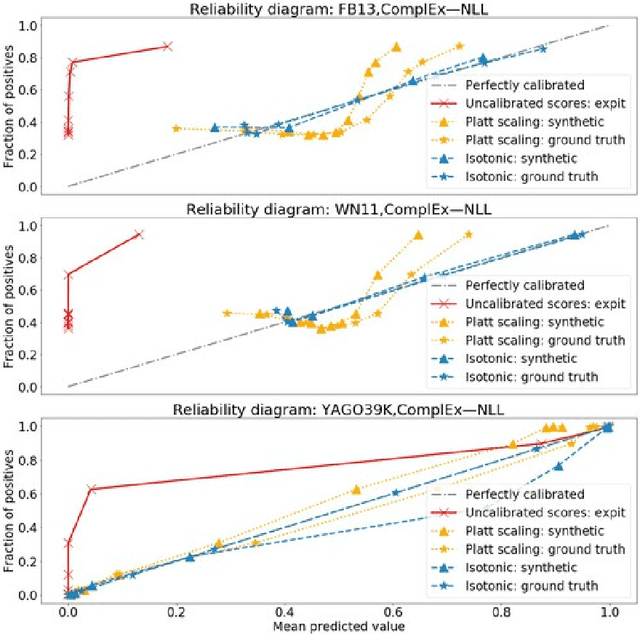

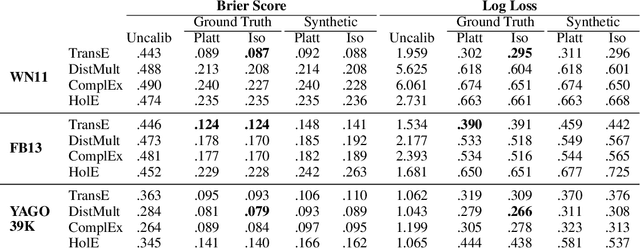

Probability Calibration for Knowledge Graph Embedding Models

Feb 13, 2020

Knowledge graph embedding research has overlooked the problem of probability calibration. We show popular embedding models are indeed uncalibrated. That means probability estimates associated to predicted triples are unreliable. We present a novel method to calibrate a model when ground truth negatives are not available, which is the usual case in knowledge graphs. We propose to use Platt scaling and isotonic regression alongside our method. Experiments on three datasets with ground truth negatives show our contribution leads to well-calibrated models when compared to the gold standard of using negatives. We get significantly better results than the uncalibrated models from all calibration methods. We show isotonic regression offers the best the performance overall, not without trade-offs. We also show that calibrated models reach state-of-the-art accuracy without the need to define relation-specific decision thresholds.

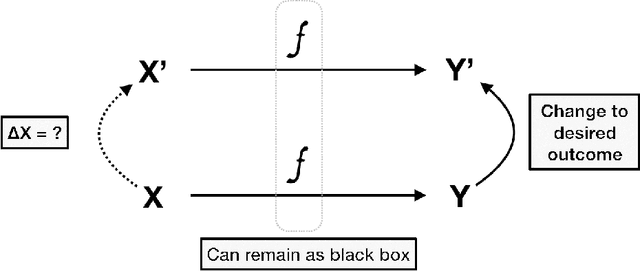

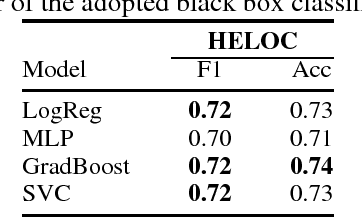

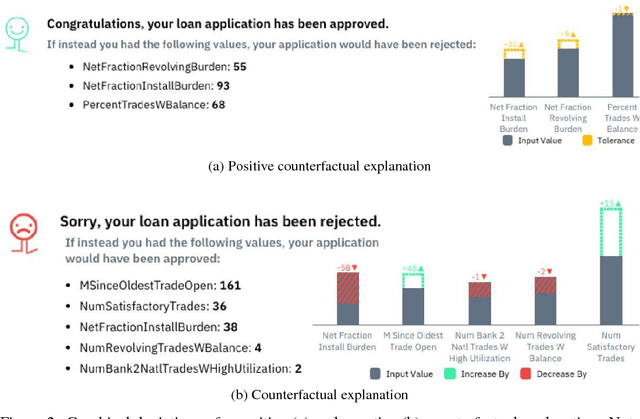

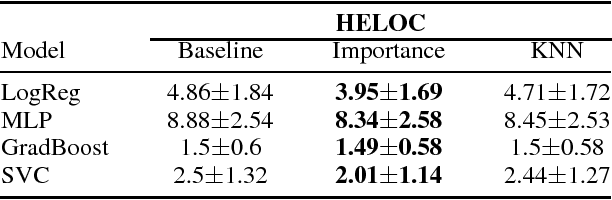

Interpretable Credit Application Predictions With Counterfactual Explanations

Nov 16, 2018

We predict credit applications with off-the-shelf, interchangeable black-box classifiers and we explain single predictions with counterfactual explanations. Counterfactual explanations expose the minimal changes required on the input data to obtain a different result e.g., approved vs rejected application. Despite their effectiveness, counterfactuals are mainly designed for changing an undesired outcome of a prediction i.e. loan rejected. Counterfactuals, however, can be difficult to interpret, especially when a high number of features are involved in the explanation. Our contribution is two-fold: i) we propose positive counterfactuals, i.e. we adapt counterfactual explanations to also explain accepted loan applications, and ii) we propose two weighting strategies to generate more interpretable counterfactuals. Experiments on the HELOC loan applications dataset show that our contribution outperforms the baseline counterfactual generation strategy, by leading to smaller and hence more interpretable counterfactuals.