Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeGenerating drawdown-realistic financial price paths using path signatures

Sep 08, 2023A novel generative machine learning approach for the simulation of sequences of financial price data with drawdowns quantifiably close to empirical data is introduced. Applications such as pricing drawdown insurance options or developing portfolio drawdown control strategies call for a host of drawdown-realistic paths. Historical scenarios may be insufficient to effectively train and backtest the strategy, while standard parametric Monte Carlo does not adequately preserve drawdowns. We advocate a non-parametric Monte Carlo approach combining a variational autoencoder generative model with a drawdown reconstruction loss function. To overcome issues of numerical complexity and non-differentiability, we approximate drawdown as a linear function of the moments of the path, known in the literature as path signatures. We prove the required regularity of drawdown function and consistency of the approximation. Furthermore, we obtain close numerical approximations using linear regression for fractional Brownian and empirical data. We argue that linear combinations of the moments of a path yield a mathematically non-trivial smoothing of the drawdown function, which gives one leeway to simulate drawdown-realistic price paths by including drawdown evaluation metrics in the learning objective. We conclude with numerical experiments on mixed equity, bond, real estate and commodity portfolios and obtain a host of drawdown-realistic paths.

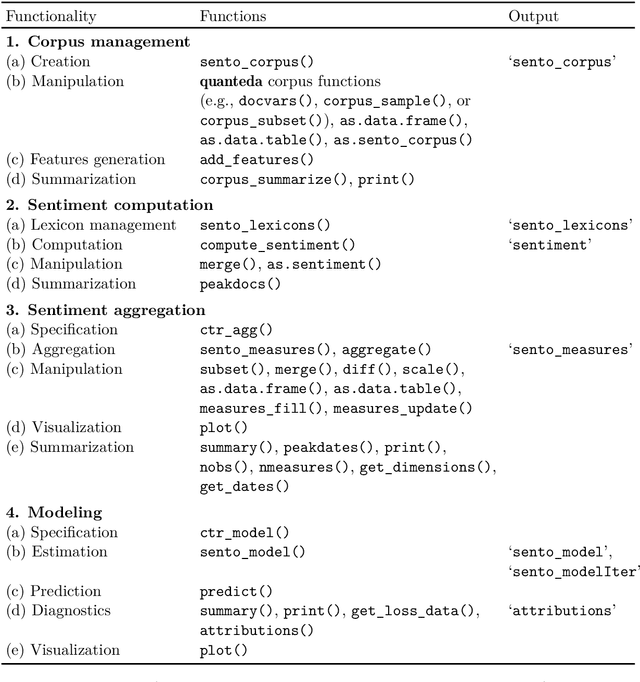

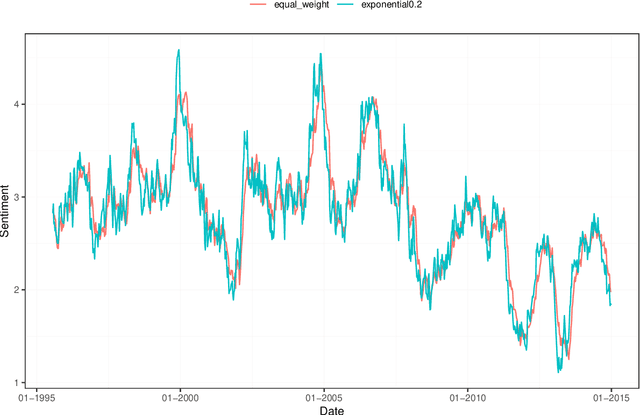

The R package sentometrics to compute, aggregate and predict with textual sentiment

Oct 20, 2021

We provide a hands-on introduction to optimized textual sentiment indexation using the R package sentometrics. Textual sentiment analysis is increasingly used to unlock the potential information value of textual data. The sentometrics package implements an intuitive framework to efficiently compute sentiment scores of numerous texts, to aggregate the scores into multiple time series, and to use these time series to predict other variables. The workflow of the package is illustrated with a built-in corpus of news articles from two major U.S. journals to forecast the CBOE Volatility Index.