Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeEconometrics of Machine Learning Methods in Economic Forecasting

Aug 21, 2023

This paper surveys the recent advances in machine learning method for economic forecasting. The survey covers the following topics: nowcasting, textual data, panel and tensor data, high-dimensional Granger causality tests, time series cross-validation, classification with economic losses.

Panel Data Nowcasting: The Case of Price-Earnings Ratios

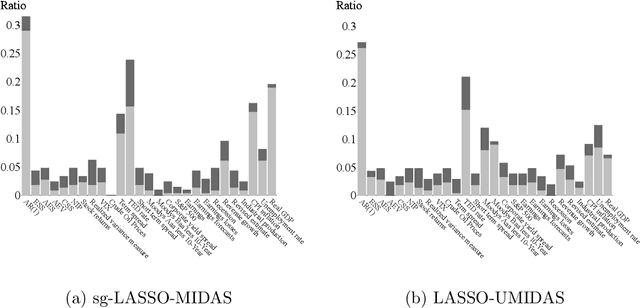

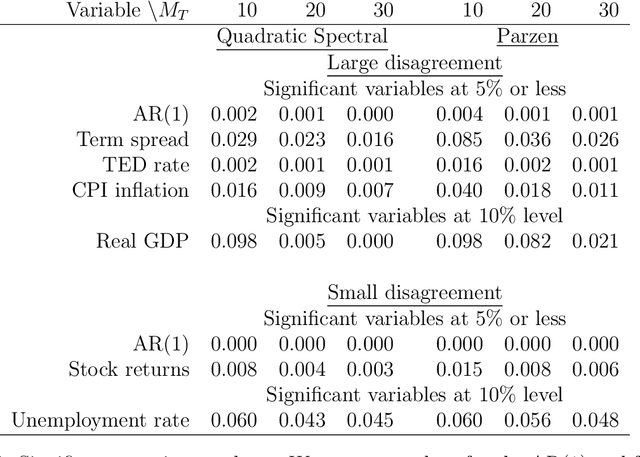

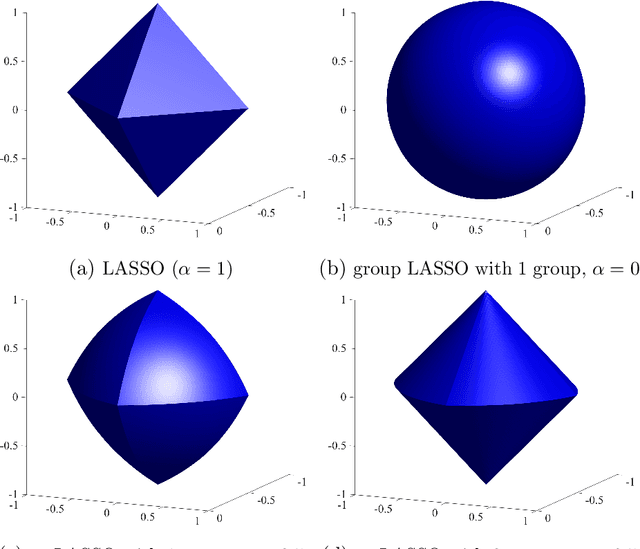

Jul 05, 2023The paper uses structured machine learning regressions for nowcasting with panel data consisting of series sampled at different frequencies. Motivated by the problem of predicting corporate earnings for a large cross-section of firms with macroeconomic, financial, and news time series sampled at different frequencies, we focus on the sparse-group LASSO regularization which can take advantage of the mixed frequency time series panel data structures. Our empirical results show the superior performance of our machine learning panel data regression models over analysts' predictions, forecast combinations, firm-specific time series regression models, and standard machine learning methods.

Machine Learning Panel Data Regressions with an Application to Nowcasting Price Earnings Ratios

Aug 08, 2020

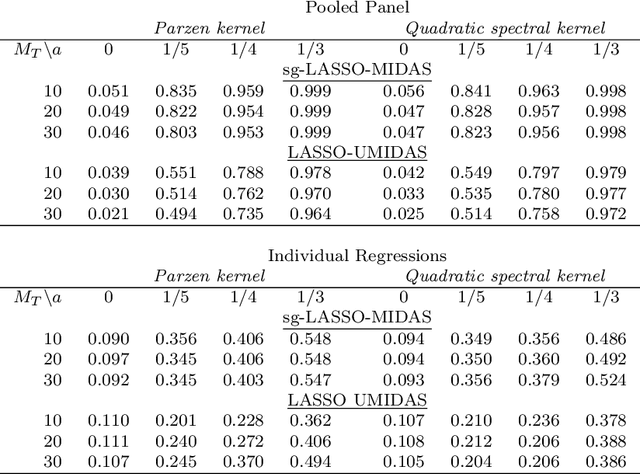

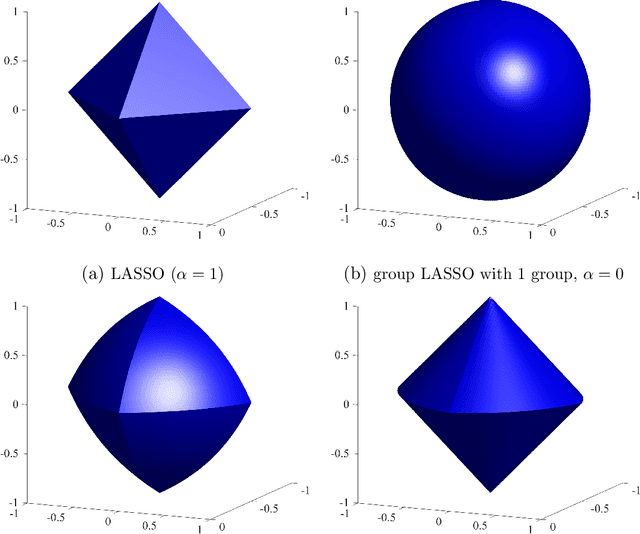

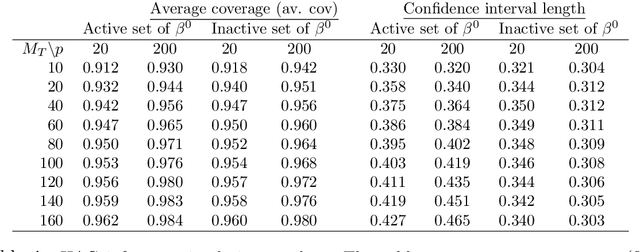

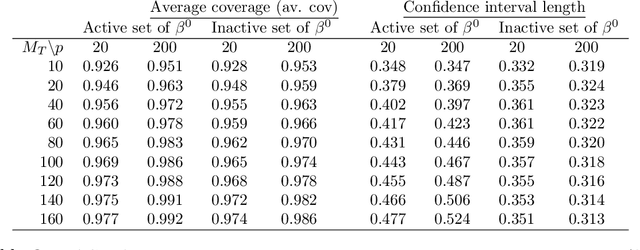

This paper introduces structured machine learning regressions for prediction and nowcasting with panel data consisting of series sampled at different frequencies. Motivated by the empirical problem of predicting corporate earnings for a large cross-section of firms with macroeconomic, financial, and news time series sampled at different frequencies, we focus on the sparse-group LASSO regularization. This type of regularization can take advantage of the mixed frequency time series panel data structures and we find that it empirically outperforms the unstructured machine learning methods. We obtain oracle inequalities for the pooled and fixed effects sparse-group LASSO panel data estimators recognizing that financial and economic data exhibit heavier than Gaussian tails. To that end, we leverage on a novel Fuk-Nagaev concentration inequality for panel data consisting of heavy-tailed $\tau$-mixing processes which may be of independent interest in other high-dimensional panel data settings.

Machine learning time series regressions with an application to nowcasting

May 29, 2020

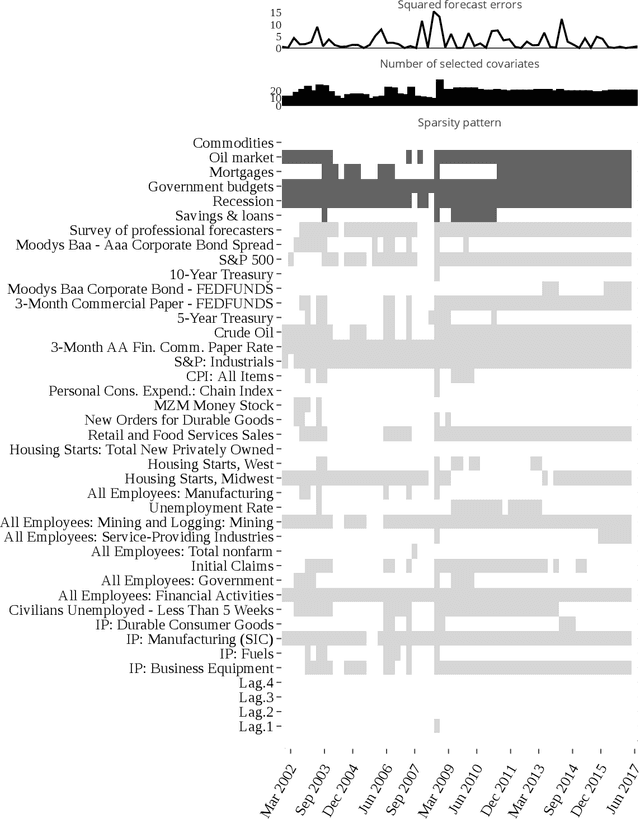

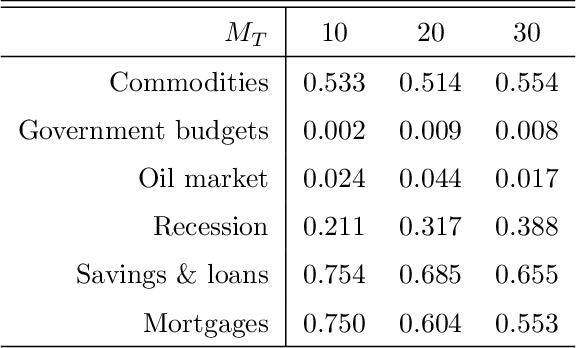

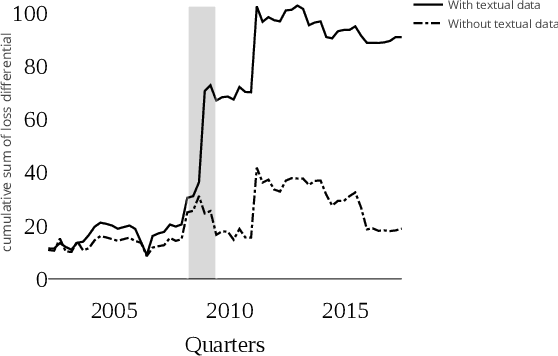

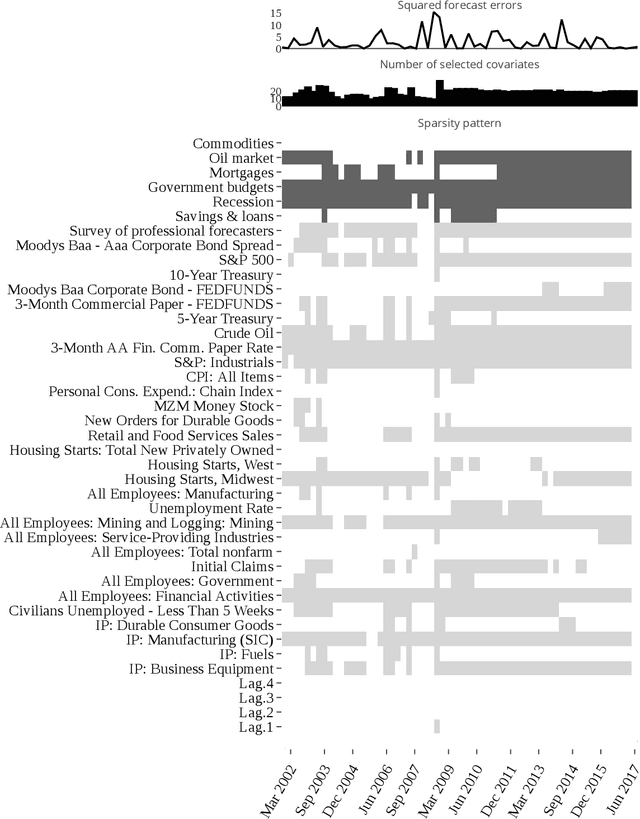

This paper introduces structured machine learning regressions for high-dimensional time series data potentially sampled at different frequencies. The sparse-group LASSO estimator can take advantage of such time series data structures and outperforms the unstructured LASSO. We establish oracle inequalities for the sparse-group LASSO estimator within a framework that allows for the mixing processes and recognizes that the financial and the macroeconomic data may have heavier than exponential tails. An empirical application to nowcasting US GDP growth indicates that the estimator performs favorably compared to other alternatives and that the text data can be a useful addition to more traditional numerical data.

Estimation and HAC-based Inference for Machine Learning Time Series Regressions

Dec 13, 2019

Time series regression analysis in econometrics typically involves a framework relying on a set of mixing conditions to establish consistency and asymptotic normality of parameter estimates and HAC-type estimators of the residual long-run variances to conduct proper inference. This article introduces structured machine learning regressions for high-dimensional time series data using the aforementioned commonly used setting. To recognize the time series data structures we rely on the sparse-group LASSO estimator. We derive a new Fuk-Nagaev inequality for a class of $\tau$-dependent processes with heavier than Gaussian tails, nesting $\alpha$-mixing processes as a special case, and establish estimation, prediction, and inferential properties, including convergence rates of the HAC estimator for the long-run variance based on LASSO residuals. An empirical application to nowcasting US GDP growth indicates that the estimator performs favorably compared to other alternatives and that the text data can be a useful addition to more traditional numerical data.