Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeImpulse Response Analysis for Sparse High-Dimensional Time Series

Jul 30, 2020

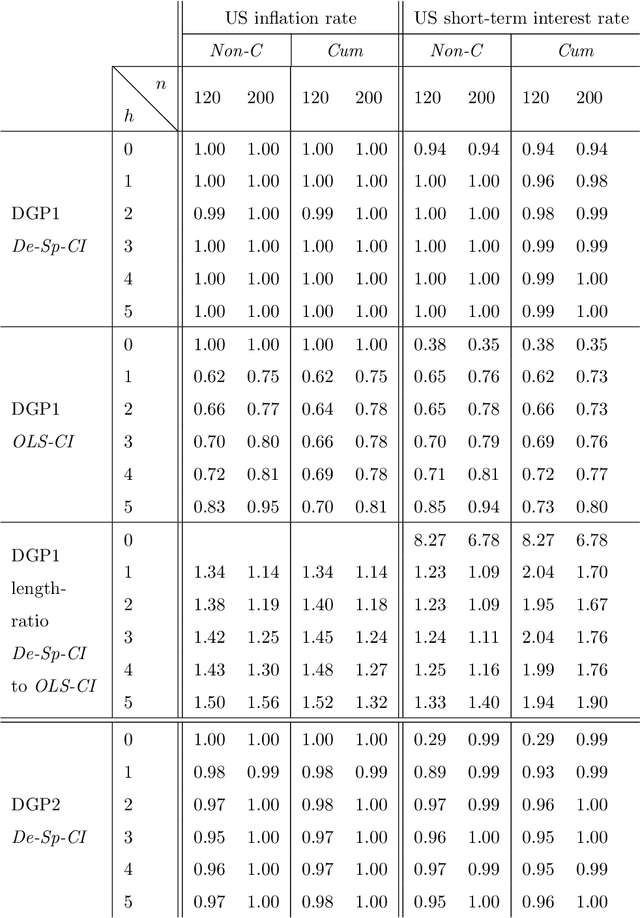

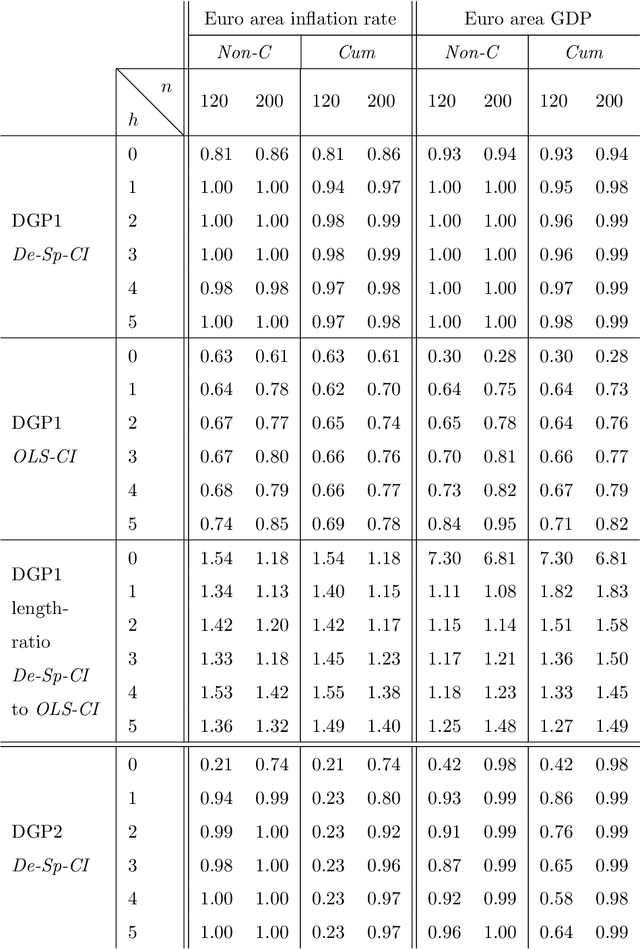

We consider structural impulse response analysis for sparse high-dimensional vector autoregressive (VAR) systems. Since standard procedures like the delta-method do not lead to valid inference in the high-dimensional set-up, we propose an alternative approach. First, we directly construct a de-sparsified version of the regularized estimators of the moving average parameters that are associated with the VAR process. Second, the obtained estimators are combined with a de-sparsified estimator of the contemporaneous impact matrix in order to estimate the structural impulse response coefficients of interest. We show that the resulting estimator of the impulse response coefficients has a Gaussian limiting distribution. Valid inference is then implemented using an appropriate bootstrap approach. Our inference procedure is illustrated by means of simulations and real data applications.

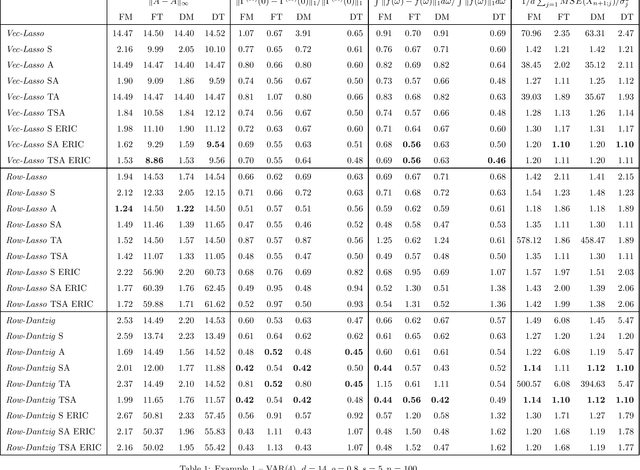

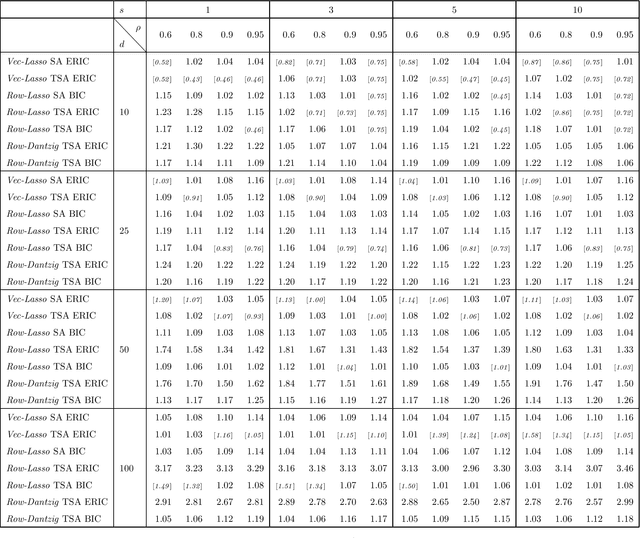

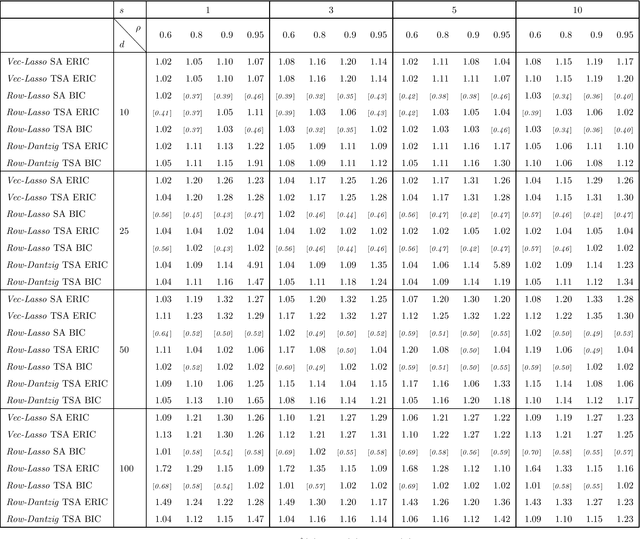

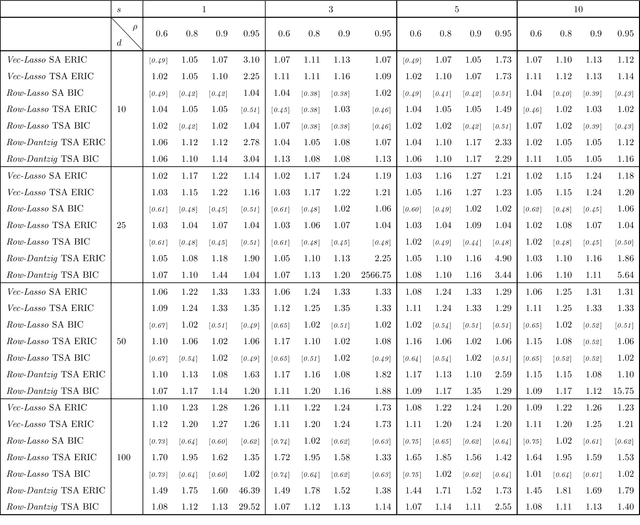

Statistical Estimation of High-Dimensional Vector Autoregressive Models

Jun 09, 2020

High-dimensional vector autoregressive (VAR) models are important tools for the analysis of multivariate time series. This paper focuses on high-dimensional time series and on the different regularized estimation procedures proposed for fitting sparse VAR models to such time series. Attention is paid to the different sparsity assumptions imposed on the VAR parameters and how these sparsity assumptions are related to the particular consistency properties of the estimators established. A sparsity scheme for high-dimensional VAR models is proposed which is found to be more appropriate for the time series setting considered. Furthermore, it is shown that, under this sparsity setting, threholding extents the consistency properties of regularized estimators to a wide range of matrix norms. Among other things, this enables application of the VAR parameters estimators to different inference problems, like forecasting or estimating the second-order characteristics of the underlying VAR process. Extensive simulations compare the finite sample behavior of the different regularized estimators proposed using a variety of performance criteria.