Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeHedging with Neural Networks

May 25, 2020

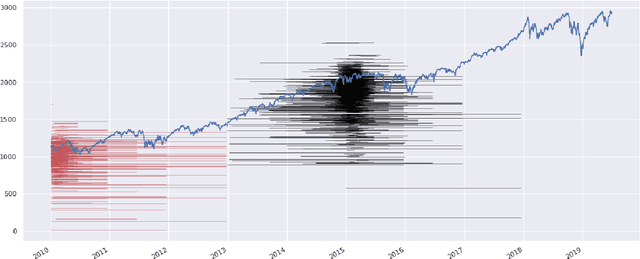

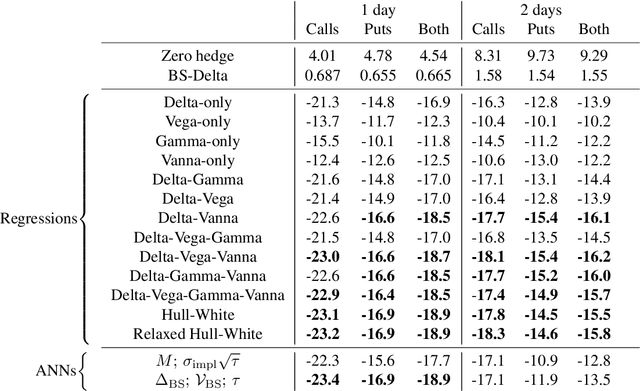

We study neural networks as nonparametric estimation tools for the hedging of options. To this end, we design a network, named HedgeNet, that directly outputs a hedging strategy. This network is trained to minimise the hedging error instead of the pricing error. Applied to end-of-day and tick prices of S&P 500 and Euro Stoxx 50 options, the network is able to reduce the mean squared hedging error of the Black-Scholes benchmark significantly. We illustrate, however, that a similar benefit arises by simple linear regressions that incorporate the leverage effect. Finally, we show how a faulty training/test data split, possibly along with an additional 'tagging' of data, leads to a significant overestimation of the outperformance of neural networks.

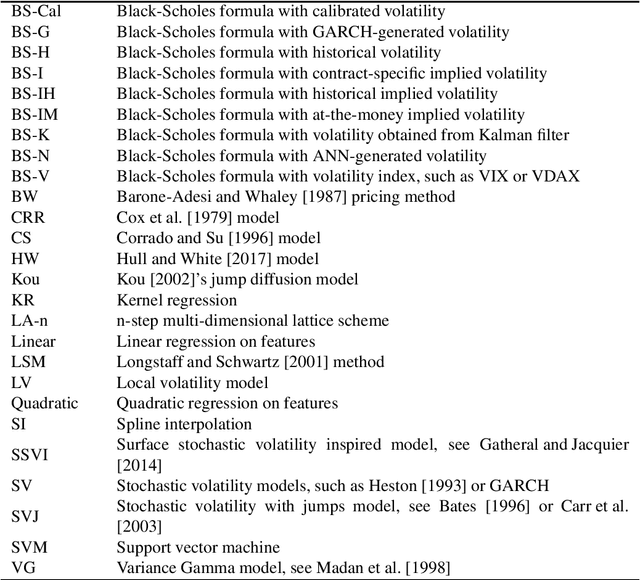

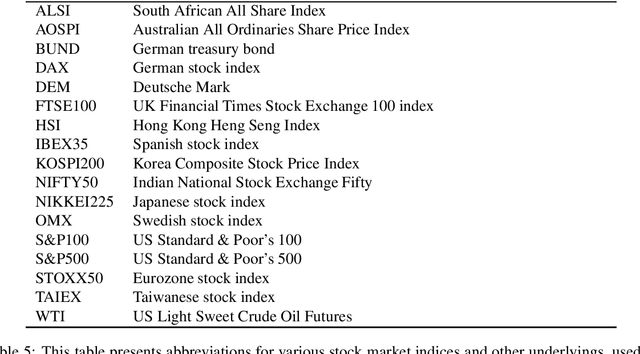

Neural networks for option pricing and hedging: a literature review

Nov 13, 2019

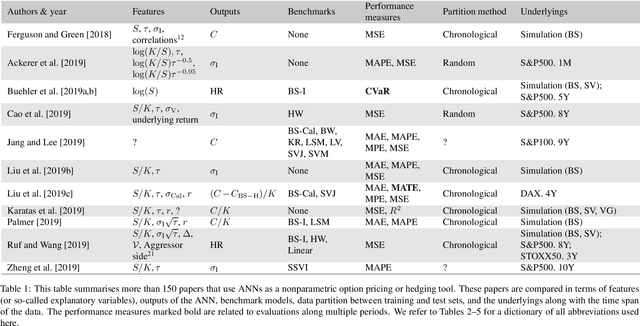

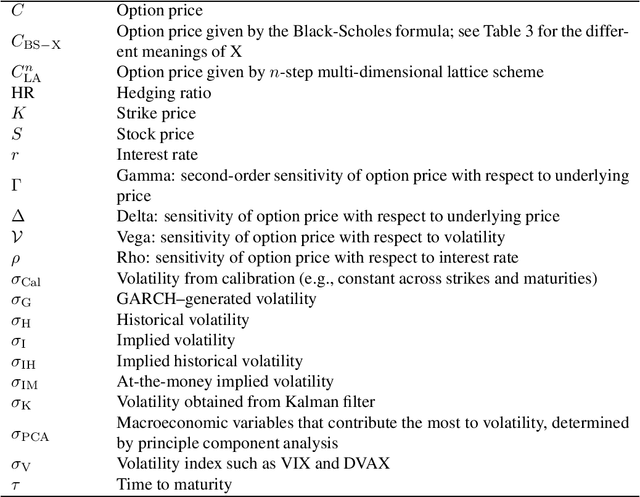

Neural networks have been used as a nonparametric method for option pricing and hedging since the early 1990s. Far over a hundred papers have been published on this topic. This note intends to provide a comprehensive review. Papers are compared in terms of input features, output variables, benchmark models, performance measures, data partition methods, and underlying assets. Furthermore, related work and regularisation techniques are discussed.