Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeCluster Regularization via a Hierarchical Feature Regression

Jul 10, 2021

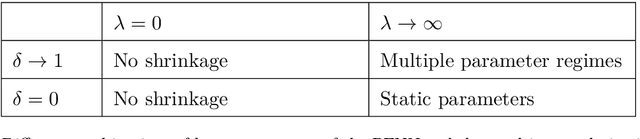

Prediction tasks with high-dimensional nonorthogonal predictor sets pose a challenge for least squares based fitting procedures. A large and productive literature exists, discussing various regularized approaches to improving the out-of-sample robustness of parameter estimates. This paper proposes a novel cluster-based regularization - the hierarchical feature regression (HFR) -, which mobilizes insights from the domains of machine learning and graph theory to estimate parameters along a supervised hierarchical representation of the predictor set, shrinking parameters towards group targets. The method is innovative in its ability to estimate optimal compositions of predictor groups, as well as the group targets endogenously. The HFR can be viewed as a supervised factor regression, with the strength of shrinkage governed by a penalty on the extent of idiosyncratic variation captured in the fitting process. The method demonstrates good predictive accuracy and versatility, outperforming a panel of benchmark regularized estimators across a diverse set of simulated regression tasks, including dense, sparse and grouped data generating processes. An application to the prediction of economic growth is used to illustrate the HFR's effectiveness in an empirical setting, with favorable comparisons to several frequentist and Bayesian alternatives.

An Interpretable Neural Network for Parameter Inference

Jun 10, 2021

Adoption of deep neural networks in fields such as economics or finance has been constrained by the lack of interpretability of model outcomes. This paper proposes a generative neural network architecture - the parameter encoder neural network (PENN) - capable of estimating local posterior distributions for the parameters of a regression model. The parameters fully explain predictions in terms of the inputs and permit visualization, interpretation and inference in the presence of complex heterogeneous effects and feature dependencies. The use of Bayesian inference techniques offers an intuitive mechanism to regularize local parameter estimates towards a stable solution, and to reduce noise-fitting in settings of limited data availability. The proposed neural network is particularly well-suited to applications in economics and finance, where parameter inference plays an important role. An application to an asset pricing problem demonstrates how the PENN can be used to explore nonlinear risk dynamics in financial markets, and to compare empirical nonlinear effects to behavior posited by financial theory.