Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDeep Portfolio Theory

Jan 14, 2018

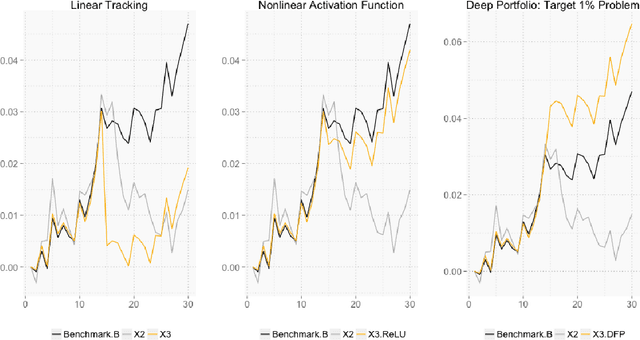

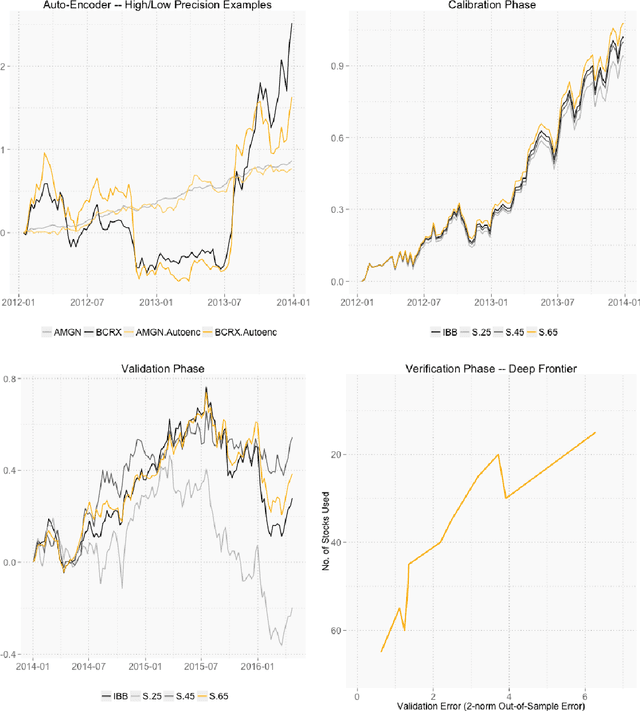

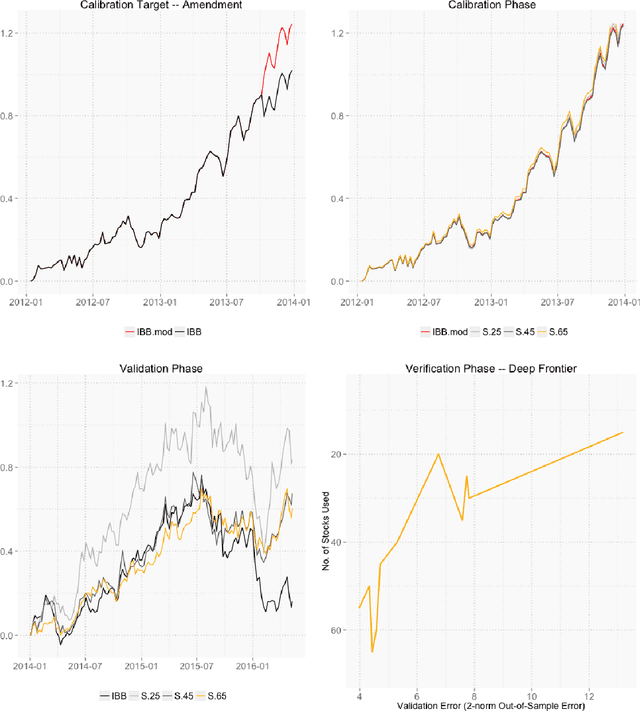

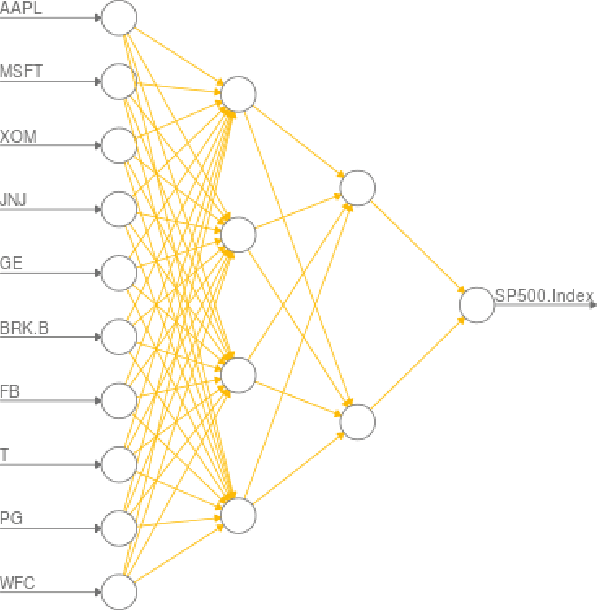

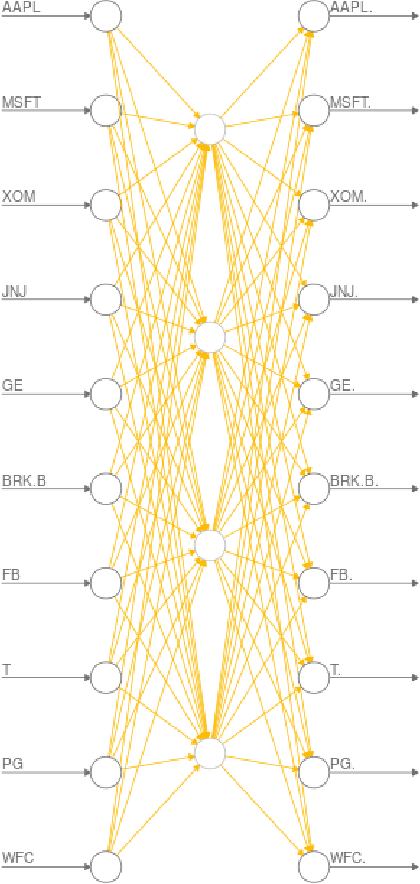

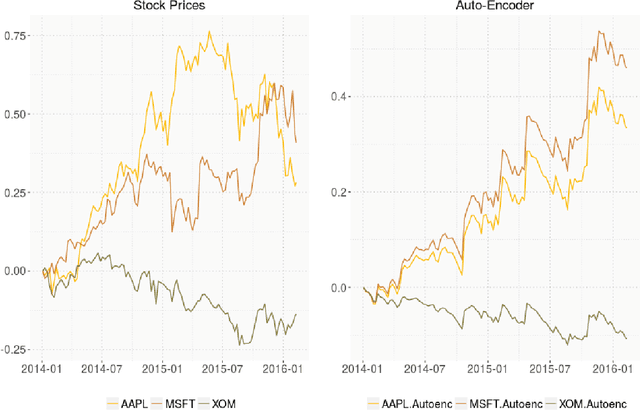

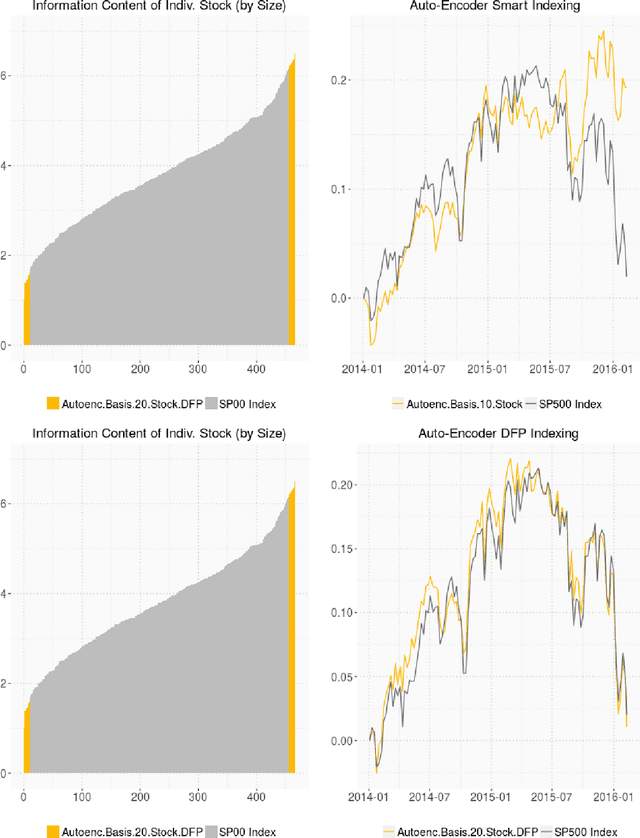

We construct a deep portfolio theory. By building on Markowitz's classic risk-return trade-off, we develop a self-contained four-step routine of encode, calibrate, validate and verify to formulate an automated and general portfolio selection process. At the heart of our algorithm are deep hierarchical compositions of portfolios constructed in the encoding step. The calibration step then provides multivariate payouts in the form of deep hierarchical portfolios that are designed to target a variety of objective functions. The validate step trades-off the amount of regularization used in the encode and calibrate steps. The verification step uses a cross validation approach to trace out an ex post deep portfolio efficient frontier. We demonstrate all four steps of our portfolio theory numerically.

Deep Learning in Finance

Jan 14, 2018

We explore the use of deep learning hierarchical models for problems in financial prediction and classification. Financial prediction problems -- such as those presented in designing and pricing securities, constructing portfolios, and risk management -- often involve large data sets with complex data interactions that currently are difficult or impossible to specify in a full economic model. Applying deep learning methods to these problems can produce more useful results than standard methods in finance. In particular, deep learning can detect and exploit interactions in the data that are, at least currently, invisible to any existing financial economic theory.