Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Dynamic Approach to Stock Price Prediction: Comparing RNN and Mixture of Experts Models Across Different Volatility Profiles

Oct 04, 2024

This study evaluates the effectiveness of a Mixture of Experts (MoE) model for stock price prediction by comparing it to a Recurrent Neural Network (RNN) and a linear regression model. The MoE framework combines an RNN for volatile stocks and a linear model for stable stocks, dynamically adjusting the weight of each model through a gating network. Results indicate that the MoE approach significantly improves predictive accuracy across different volatility profiles. The RNN effectively captures non-linear patterns for volatile companies but tends to overfit stable data, whereas the linear model performs well for predictable trends. The MoE model's adaptability allows it to outperform each individual model, reducing errors such as Mean Squared Error (MSE) and Mean Absolute Error (MAE). Future work should focus on enhancing the gating mechanism and validating the model with real-world datasets to optimize its practical applicability.

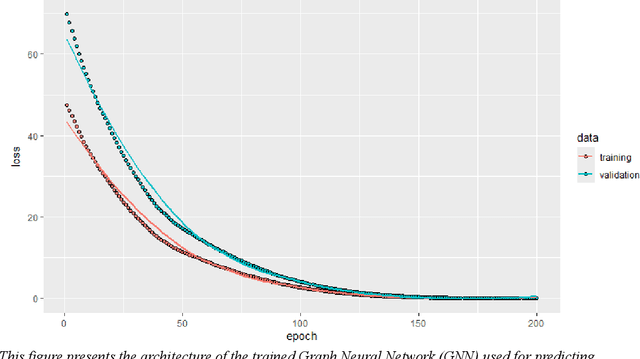

Dynamic Portfolio Rebalancing: A Hybrid new Model Using GNNs and Pathfinding for Cost Efficiency

Oct 02, 2024

This paper introduces a novel approach to optimizing portfolio rebalancing by integrating Graph Neural Networks (GNNs) for predicting transaction costs and Dijkstra's algorithm for identifying cost-efficient rebalancing paths. Using historical stock data from prominent technology firms, the GNN is trained to forecast future transaction costs, which are then applied as edge weights in a financial asset graph. Dijkstra's algorithm is used to find the least costly path for reallocating capital between assets. Empirical results show that this hybrid approach significantly reduces transaction costs, offering a powerful tool for portfolio managers, especially in high-frequency trading environments. This methodology demonstrates the potential of combining advanced machine learning techniques with classical optimization algorithms to improve financial decision-making processes. Future research will explore expanding the asset universe and incorporating reinforcement learning for continuous portfolio optimization.

Analyzing Economic Convergence Across the Americas: A Survival Analysis Approach to GDP per Capita Trajectories

Apr 03, 2024By integrating survival analysis, machine learning algorithms, and economic interpretation, this research examines the temporal dynamics associated with attaining a 5 percent rise in purchasing power parity-adjusted GDP per capita over a period of 120 months (2013-2022). A comparative investigation reveals that DeepSurv is proficient at capturing non-linear interactions, although standard models exhibit comparable performance under certain circumstances. The weight matrix evaluates the economic ramifications of vulnerabilities, risks, and capacities. In order to meet the GDPpc objective, the findings emphasize the need of a balanced approach to risk-taking, strategic vulnerability reduction, and investment in governmental capacities and social cohesiveness. Policy guidelines promote individualized approaches that take into account the complex dynamics at play while making decisions.

Buy when? Survival machine learning model comparison for purchase timing

Aug 28, 2023The value of raw data is unlocked by converting it into information and knowledge that drives decision-making. Machine Learning (ML) algorithms are capable of analysing large datasets and making accurate predictions. Market segmentation, client lifetime value, and marketing techniques have all made use of machine learning. This article examines marketing machine learning techniques such as Support Vector Machines, Genetic Algorithms, Deep Learning, and K-Means. ML is used to analyse consumer behaviour, propose items, and make other customer choices about whether or not to purchase a product or service, but it is seldom used to predict when a person will buy a product or a basket of products. In this paper, the survival models Kernel SVM, DeepSurv, Survival Random Forest, and MTLR are examined to predict tine-purchase individual decisions. Gender, Income, Location, PurchaseHistory, OnlineBehavior, Interests, PromotionsDiscounts and CustomerExperience all have an influence on purchasing time, according to the analysis. The study shows that the DeepSurv model predicted purchase completion the best. These insights assist marketers in increasing conversion rates.