Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMaking Good on LSTMs' Unfulfilled Promise

Dec 09, 2019

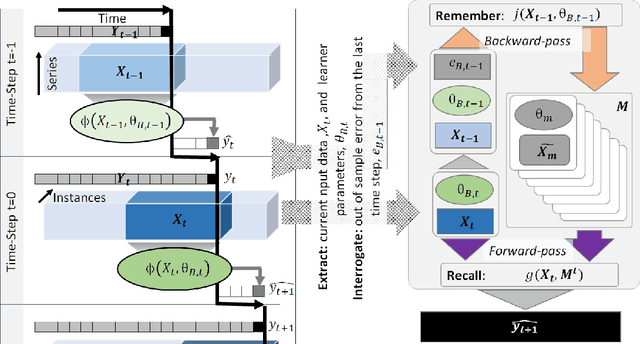

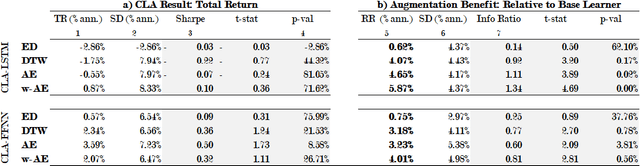

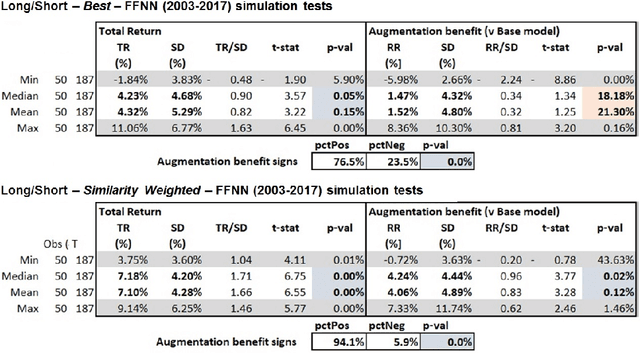

LSTMs promise much to financial time-series analysis, temporal and cross-sectional inference, but we find that they do not deliver in a real-world financial management task. We examine an alternative called Continual Learning (CL), a memory-augmented approach, which can provide transparent explanations, i.e. which memory did what and when. This work has implications for many financial applications including credit, time-varying fairness in decision making and more. We make three important new observations. Firstly, as well as being more explainable, time-series CL approaches outperform LSTMs as well as a simple sliding window learner using feed-forward neural networks (FFNN). Secondly, we show that CL based on a sliding window learner (FFNN) is more effective than CL based on a sequential learner (LSTM). Thirdly, we examine how real-world, time-series noise impacts several similarity approaches used in CL memory addressing. We provide these insights using an approach called Continual Learning Augmentation (CLA) tested on a complex real-world problem, emerging market equities investment decision making. CLA provides a test-bed as it can be based on different types of time-series learners, allowing testing of LSTM and FFNN learners side by side. CLA is also used to test several distance approaches used in a memory recall-gate: Euclidean distance (ED), dynamic time warping (DTW), auto-encoders (AE) and a novel hybrid approach, warp-AE. We find that ED under-performs DTW and AE but warp-AE shows the best overall performance in a real-world financial task.

Continual Learning Augmented Investment Decisions

Dec 14, 2018

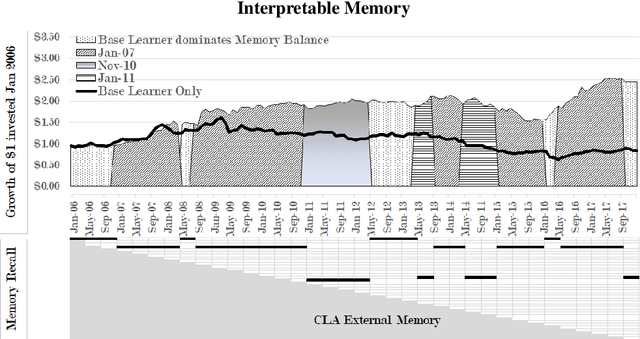

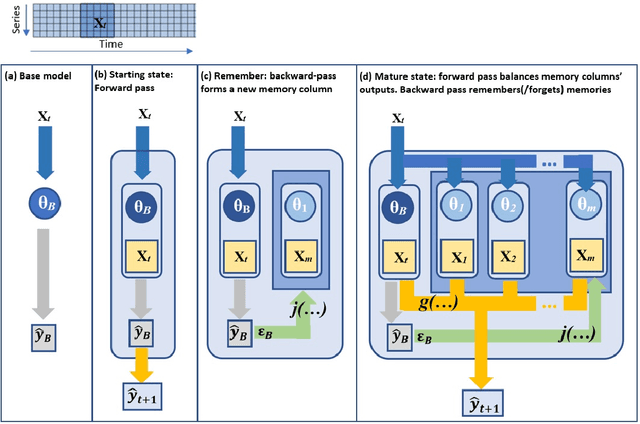

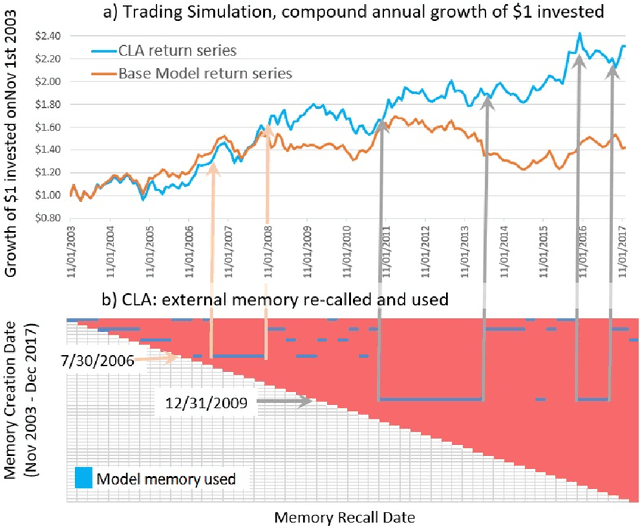

Investment decisions can benefit from incorporating an accumulated knowledge of the past to drive future decision making. We introduce Continual Learning Augmentation (CLA) which is based on an explicit memory structure and a feed forward neural network (FFNN) base model and used to drive long term financial investment decisions. We demonstrate that our approach improves accuracy in investment decision making while memory is addressed in an explainable way. Our approach introduces novel remember cues, consisting of empirically learned change points in the absolute error series of the FFNN. Memory recall is also novel, with contextual similarity assessed over time by sampling distances using dynamic time warping (DTW). We demonstrate the benefits of our approach by using it in an expected return forecasting task to drive investment decisions. In an investment simulation in a broad international equity universe between 2003-2017, our approach significantly outperforms FFNN base models. We also illustrate how CLA's memory addressing works in practice, using a worked example to demonstrate the explainability of our approach.