Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeBayesian Conditional Cointegration

Jun 27, 2012

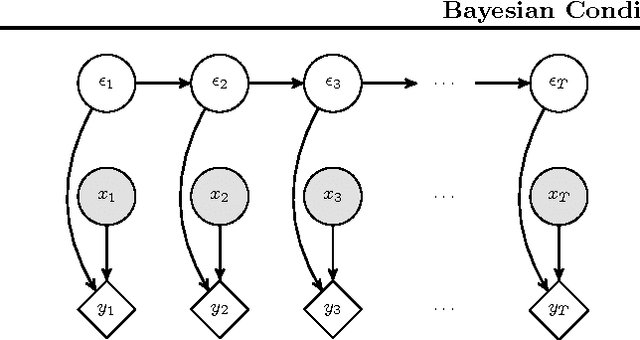

Cointegration is an important topic for time-series, and describes a relationship between two series in which a linear combination is stationary. Classically, the test for cointegration is based on a two stage process in which first the linear relation between the series is estimated by Ordinary Least Squares. Subsequently a unit root test is performed on the residuals. A well-known deficiency of this classical approach is that it can lead to erroneous conclusions about the presence of cointegration. As an alternative, we present a framework for estimating whether cointegration exists using Bayesian inference which is empirically superior to the classical approach. Finally, we apply our technique to model segmented cointegration in which cointegration may exist only for limited time. In contrast to previous approaches our model makes no restriction on the number of possible cointegration segments.