Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeApplying separative non-negative matrix factorization to extra-financial data

Jun 09, 2022

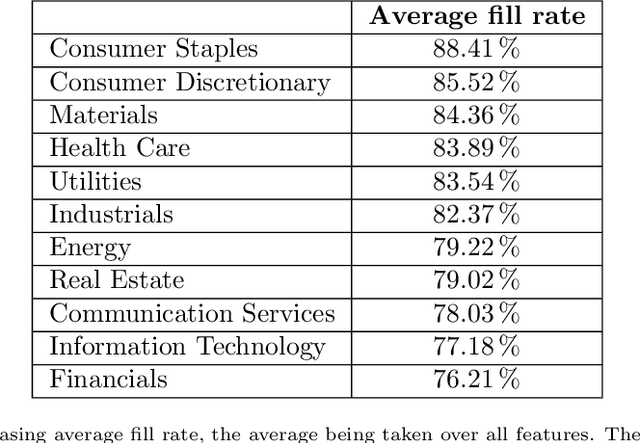

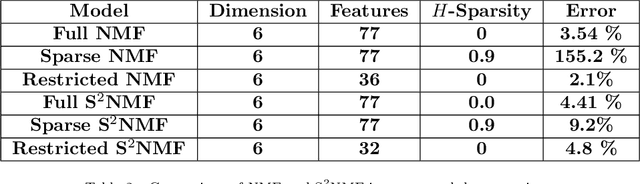

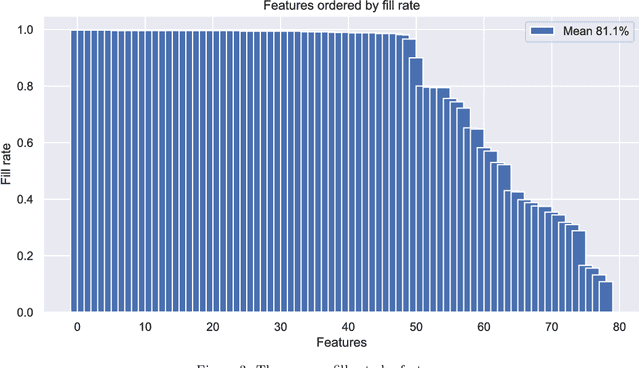

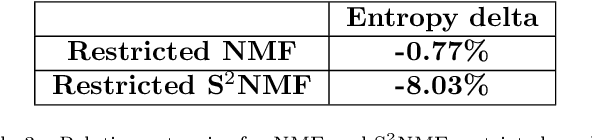

We present here an original application of the non-negative matrix factorization (NMF) method, for the case of extra-financial data. These data are subject to high correlations between co-variables, as well as between observations. NMF provides a much more relevant clustering of co-variables and observations than a simple principal component analysis (PCA). In addition, we show that an initial data separation step before applying NMF further improves the quality of the clustering.

Online Bayesian inference for multiple changepoints and risk assessment

May 31, 2021The aim of the present study is to detect abrupt trend changes in the mean of a multidimensional sequential signal. Directly inspired by papers of Fernhead and Liu ([4] and [5]), this work describes the signal in a hierarchical manner : the change dates of a time segmentation process trigger the renewal of a piece-wise constant emission law. Bayesian posterior information on the change dates and emission parameters is obtained. These estimations can be revised online, i.e. as new data arrive. This paper proposes explicit formulations corresponding to various emission laws, as well as a generalization to the case where only partially observed data are available. Practical applications include the returns of partially observed multi-asset investment strategies, when only scant prior knowledge of the movers of the returns is at hand, limited to some statistical assumptions. This situation is different from the study of trend changes in the returns of individual assets, where fundamental exogenous information (news, earnings announcements, controversies, etc.) can be used.