Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMachine Learning for Biomedical Raman Spectroscopy: From Spectral Acquisition to Clinical Translation

Jun 12, 2026Raman spectroscopy provides label-free, chemically specific characterization of biological systems and has become an important tool for cancer diagnosis, molecular subtyping, microbiological identification, and intraoperative decision support. Biomedical Raman spectra are, however, high-dimensional, noisy, and affected by fluorescence background, acquisition variability, and biological heterogeneity, making robust computational analysis essential. This review examines the role of machine learning across the biomedical Raman spectroscopy pipeline, from preprocessing and signal correction to unsupervised structure discovery, supervised diagnosis and molecular stratification, representation and transfer learning, explainability, biomarker discovery, and multimodal integration with imaging, pathology, and molecular profiling. Emphasis is placed on the use of machine learning not only for diagnostic classification, but also for biologically interpretable and clinically actionable analysis. We also discuss the main barriers to clinical translation, including limited dataset sizes, inter-instrument variability, inconsistent preprocessing, insufficient external validation, reproducibility concerns, and limited sharing of software, data, and metadata. We argue that progress will require methodological advances together with standardization, robust validation, explainability, and deployment-ready analytical frameworks. By integrating methodological, biomedical, and translational perspectives, this review outlines key directions for developing reliable and clinically deployable Raman-AI systems.

Advancing GDP Forecasting: The Potential of Machine Learning Techniques in Economic Predictions

Feb 27, 2025The quest for accurate economic forecasting has traditionally been dominated by econometric models, which most of the times rely on the assumptions of linear relationships and stationarity in of the data. However, the complex and often nonlinear nature of global economies necessitates the exploration of alternative approaches. Machine learning methods offer promising advantages over traditional econometric techniques for Gross Domestic Product forecasting, given their ability to model complex, nonlinear interactions and patterns without the need for explicit specification of the underlying relationships. This paper investigates the efficacy of Recurrent Neural Networks, in forecasting GDP, specifically LSTM networks. These models are compared against a traditional econometric method, SARIMA. We employ the quarterly Romanian GDP dataset from 1995 to 2023 and build a LSTM network to forecast to next 4 values in the series. Our findings suggest that machine learning models, consistently outperform traditional econometric models in terms of predictive accuracy and flexibility

Text classification using machine learning methods

Feb 27, 2025

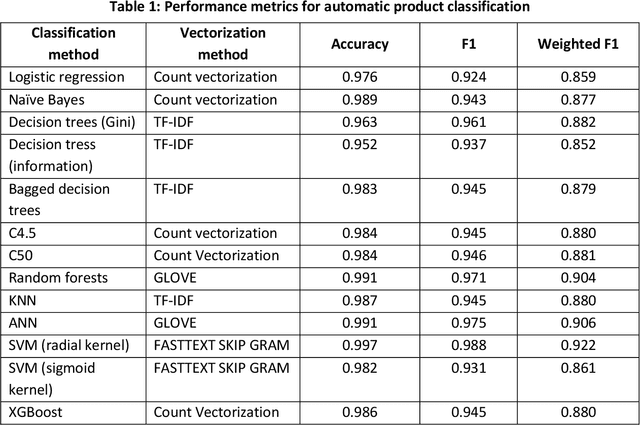

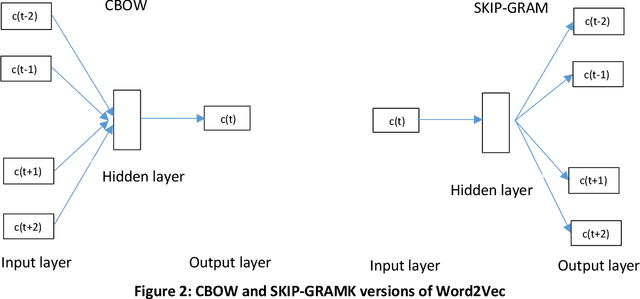

In this paper we present the results of an experiment aimed to use machine learning methods to obtain models that can be used for the automatic classification of products. In order to apply automatic classification methods, we transformed the product names from a text representation to numeric vectors, a process called word embedding. We used several embedding methods: Count Vectorization, TF-IDF, Word2Vec, FASTTEXT, and GloVe. Having the product names in a form of numeric vectors, we proceeded with a set of machine learning methods for automatic classification: Logistic Regression, Multinomial Naive Bayes, kNN, Artificial Neural Networks, Support Vector Machines, and Decision trees with several variants. The results show an impressive accuracy of the classification process for Support Vector Machines, Logistic Regression, and Random Forests. Regarding the word embedding methods, the best results were obtained with the FASTTEXT technique.

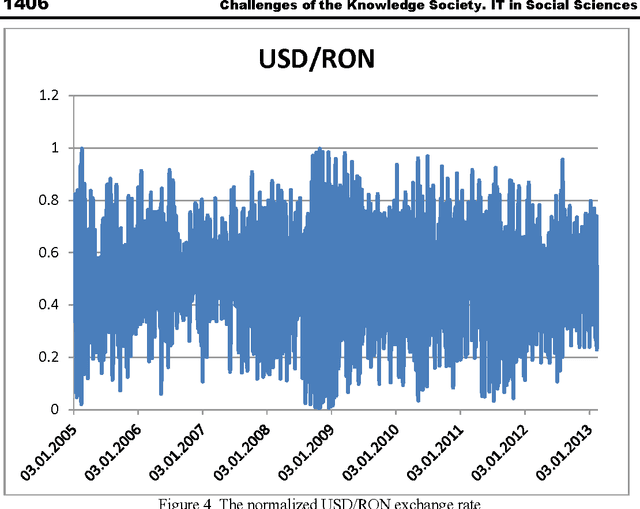

Time series forecasting using neural networks

Jan 07, 2014

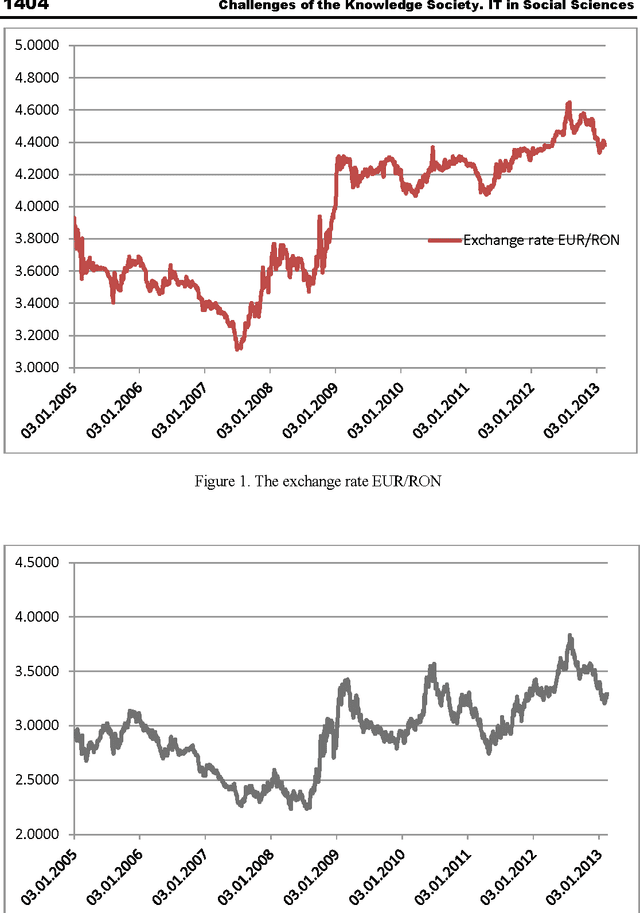

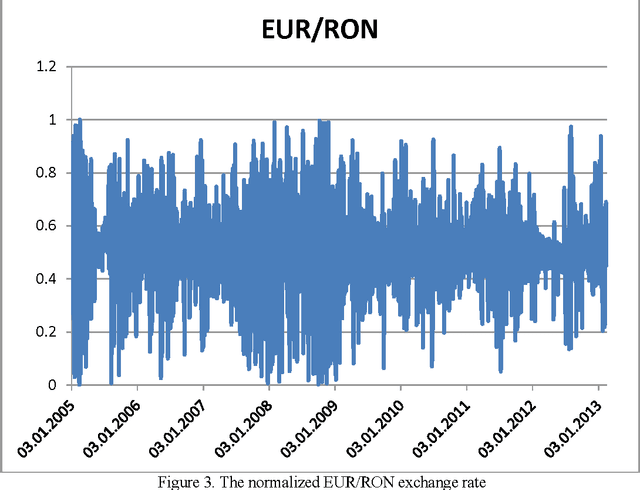

Recent studies have shown the classification and prediction power of the Neural Networks. It has been demonstrated that a NN can approximate any continuous function. Neural networks have been successfully used for forecasting of financial data series. The classical methods used for time series prediction like Box-Jenkins or ARIMA assumes that there is a linear relationship between inputs and outputs. Neural Networks have the advantage that can approximate nonlinear functions. In this paper we compared the performances of different feed forward and recurrent neural networks and training algorithms for predicting the exchange rate EUR/RON and USD/RON. We used data series with daily exchange rates starting from 2005 until 2013.

* Proceedings of the CKS 2013 International Conference