Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMeta-Learning and Meta-Reinforcement Learning - Tracing the Path towards DeepMind's Adaptive Agent

Feb 23, 2026Humans are highly effective at utilizing prior knowledge to adapt to novel tasks, a capability that standard machine learning models struggle to replicate due to their reliance on task-specific training. Meta-learning overcomes this limitation by allowing models to acquire transferable knowledge from various tasks, enabling rapid adaptation to new challenges with minimal data. This survey provides a rigorous, task-based formalization of meta-learning and meta-reinforcement learning and uses that paradigm to chronicle the landmark algorithms that paved the way for DeepMind's Adaptive Agent, consolidating the essential concepts needed to understand the Adaptive Agent and other generalist approaches.

A Reinforcement Learning Approach for the Continuous Electricity Market of Germany: Trading from the Perspective of a Wind Park Operator

Nov 26, 2021

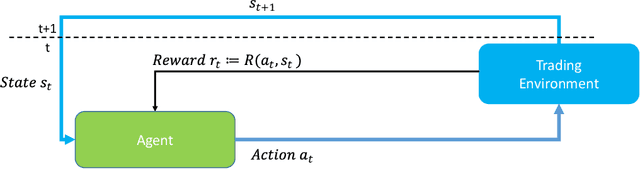

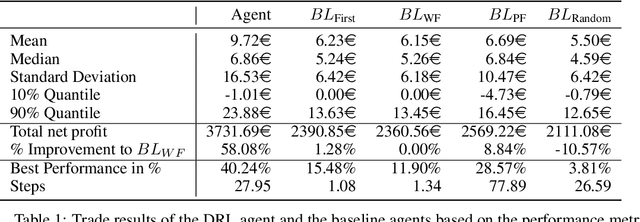

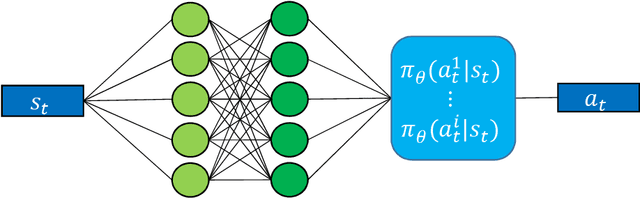

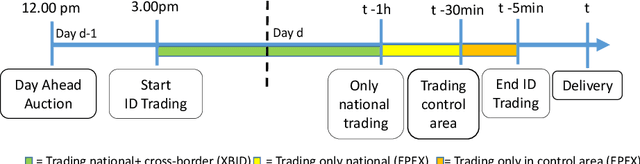

With the rising extension of renewable energies, the intraday electricity markets have recorded a growing popularity amongst traders as well as electric utilities to cope with the induced volatility of the energy supply. Through their short trading horizon and continuous nature, the intraday markets offer the ability to adjust trading decisions from the day-ahead market or reduce trading risk in a short-term notice. Producers of renewable energies utilize the intraday market to lower their forecast risk, by modifying their provided capacities based on current forecasts. However, the market dynamics are complex due to the fact that the power grids have to remain stable and electricity is only partly storable. Consequently, robust and intelligent trading strategies are required that are capable to operate in the intraday market. In this work, we propose a novel autonomous trading approach based on Deep Reinforcement Learning (DRL) algorithms as a possible solution. For this purpose, we model the intraday trade as a Markov Decision Problem (MDP) and employ the Proximal Policy Optimization (PPO) algorithm as our DRL approach. A simulation framework is introduced that enables the trading of the continuous intraday price in a resolution of one minute steps. We test our framework in a case study from the perspective of a wind park operator. We include next to general trade information both price and wind forecasts. On a test scenario of German intraday trading results from 2018, we are able to outperform multiple baselines with at least 45.24% improvement, showing the advantage of the DRL algorithm. However, we also discuss limitations and enhancements of the DRL agent, in order to increase the performance in future works.