Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAdversarial Attacks on Image Classification Models: Analysis and Defense

Dec 28, 2023The notion of adversarial attacks on image classification models based on convolutional neural networks (CNN) is introduced in this work. To classify images, deep learning models called CNNs are frequently used. However, when the networks are subject to adversarial attacks, extremely potent and previously trained CNN models that perform quite effectively on image datasets for image classification tasks may perform poorly. In this work, one well-known adversarial attack known as the fast gradient sign method (FGSM) is explored and its adverse effects on the performances of image classification models are examined. The FGSM attack is simulated on three pre-trained image classifier CNN architectures, ResNet-101, AlexNet, and RegNetY 400MF using randomly chosen images from the ImageNet dataset. The classification accuracies of the models are computed in the absence and presence of the attack to demonstrate the detrimental effect of the attack on the performances of the classifiers. Finally, a mechanism is proposed to defend against the FGSM attack based on a modified defensive distillation-based approach. Extensive results are presented for the validation of the proposed scheme.

Stock Volatility Prediction using Time Series and Deep Learning Approach

Oct 05, 2022

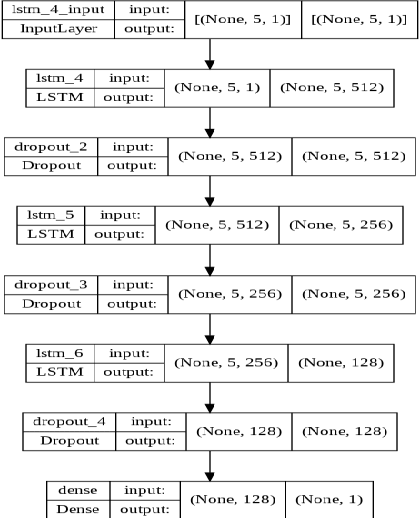

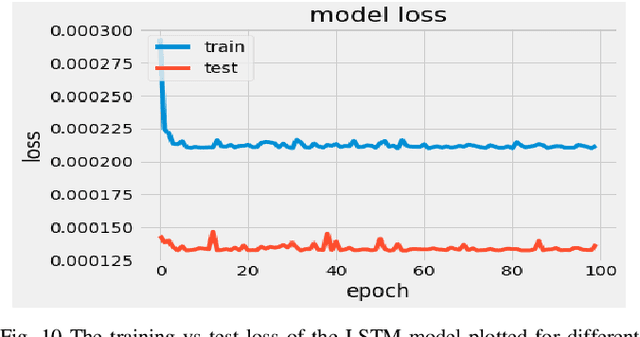

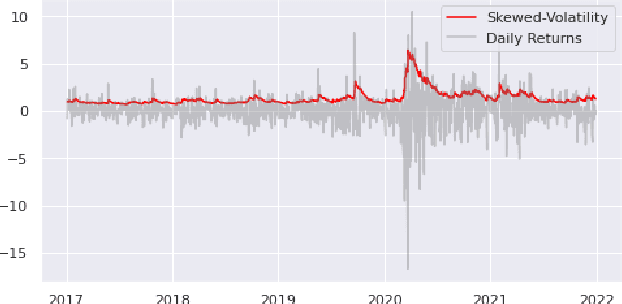

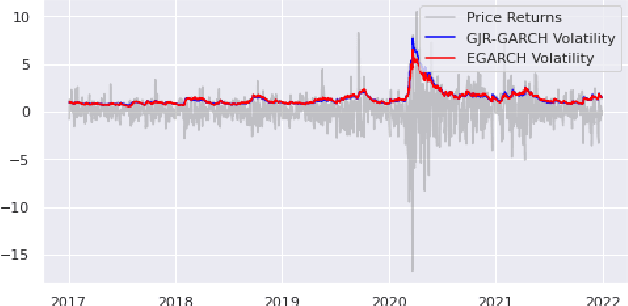

Volatility clustering is a crucial property that has a substantial impact on stock market patterns. Nonetheless, developing robust models for accurately predicting future stock price volatility is a difficult research topic. For predicting the volatility of three equities listed on India's national stock market (NSE), we propose multiple volatility models depending on the generalized autoregressive conditional heteroscedasticity (GARCH), Glosten-Jagannathan-GARCH (GJR-GARCH), Exponential general autoregressive conditional heteroskedastic (EGARCH), and LSTM framework. Sector-wise stocks have been chosen in our study. The sectors which have been considered are banking, information technology (IT), and pharma. yahoo finance has been used to obtain stock price data from Jan 2017 to Dec 2021. Among the pulled-out records, the data from Jan 2017 to Dec 2020 have been taken for training, and data from 2021 have been chosen for testing our models. The performance of predicting the volatility of stocks of three sectors has been evaluated by implementing three different types of GARCH models as well as by the LSTM model are compared. It has been observed the LSTM performed better in predicting volatility in pharma over banking and IT sectors. In tandem, it was also observed that E-GARCH performed better in the case of the banking sector and for IT and pharma, GJR-GARCH performed better.

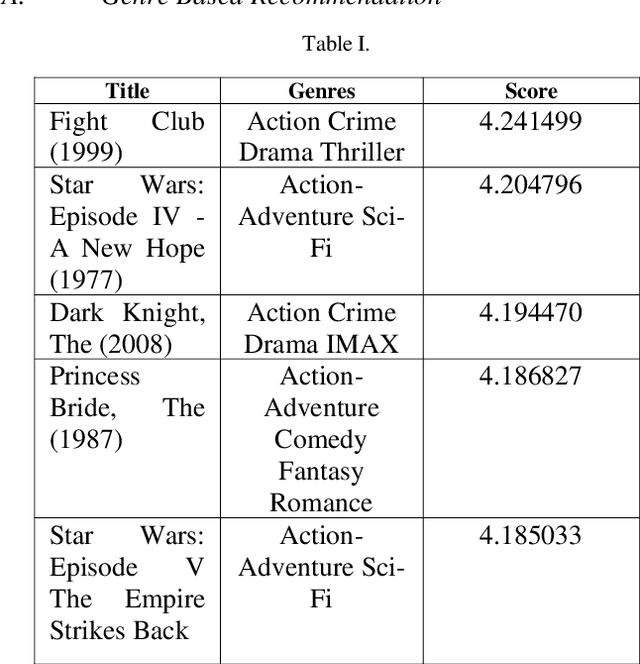

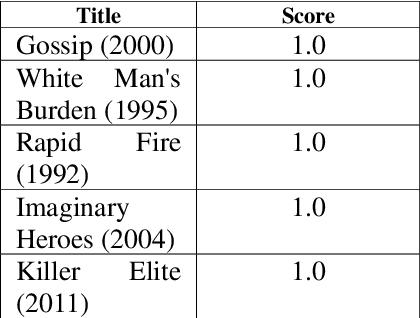

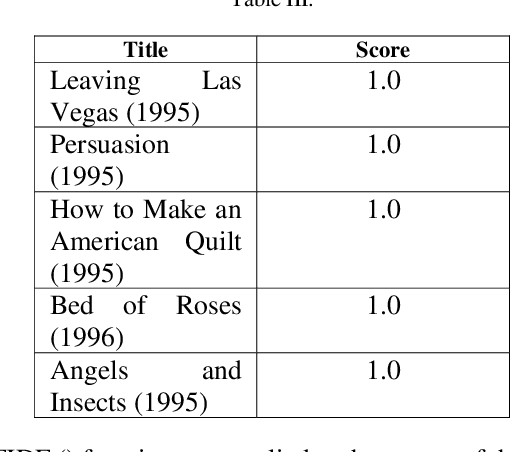

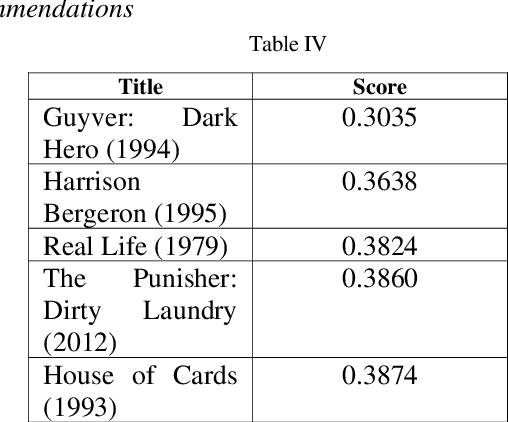

Comprehensive Movie Recommendation System

Dec 23, 2021

A recommender system, also known as a recommendation system, is a type of information filtering system that attempts to forecast a user's rating or preference for an item. This article designs and implements a complete movie recommendation system prototype based on the Genre, Pearson Correlation Coefficient, Cosine Similarity, KNN-Based, Content-Based Filtering using TFIDF and SVD, Collaborative Filtering using TFIDF and SVD, Surprise Library based recommendation system technology. Apart from that in this paper, we present a novel idea that applies machine learning techniques to construct a cluster for the movie based on genres and then observes the inertia value number of clusters were defined. The constraints of the approaches discussed in this work have been described, as well as how one strategy overcomes the disadvantages of another. The whole work has been done on the dataset Movie Lens present at the group lens website which contains 100836 ratings and 3683 tag applications across 9742 movies. These data were created by 610 users between March 29, 1996, and September 24, 2018.

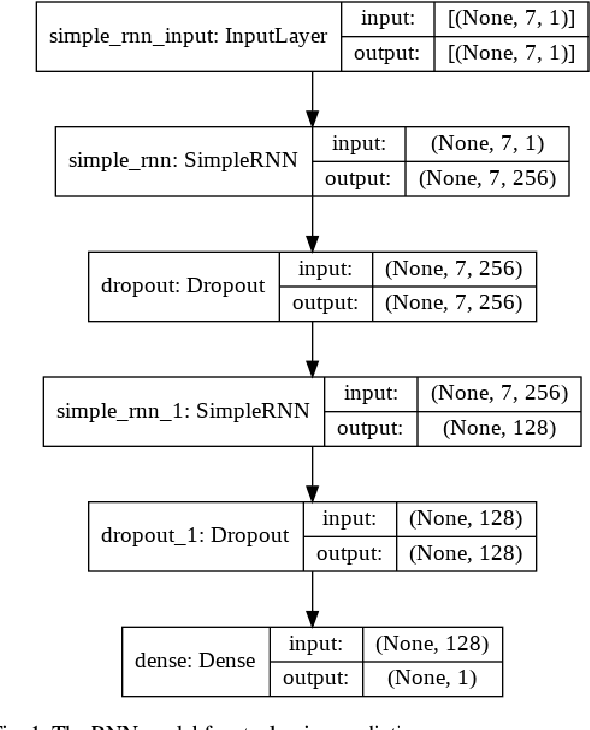

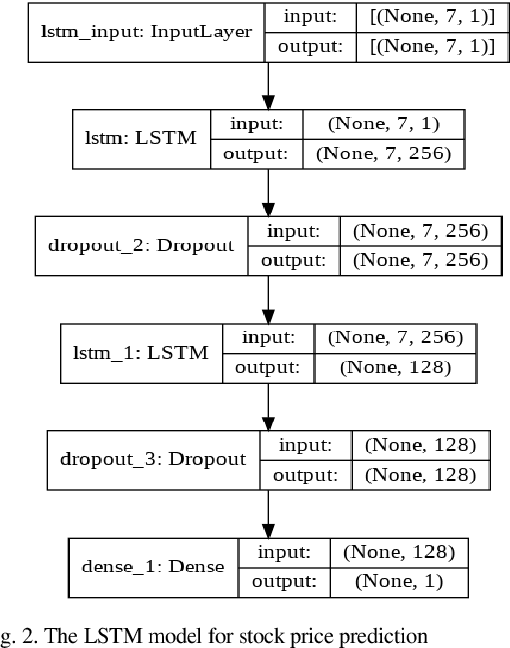

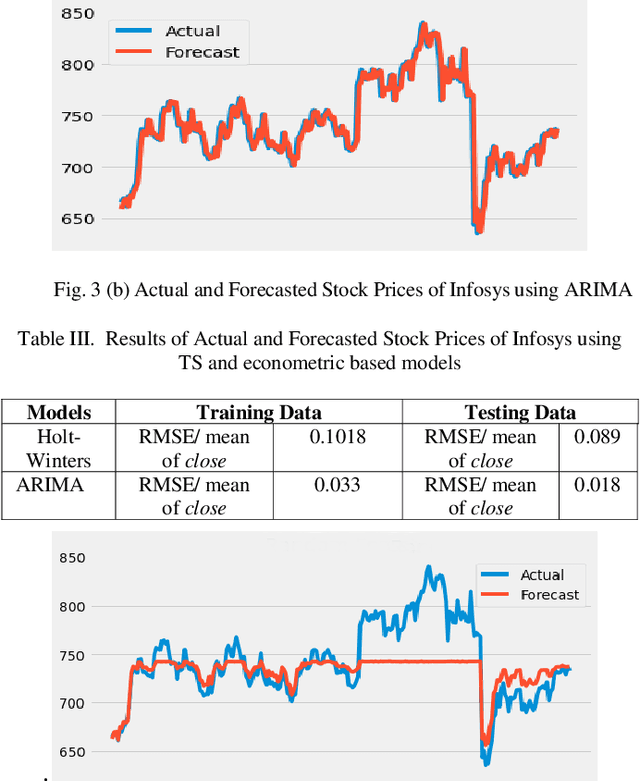

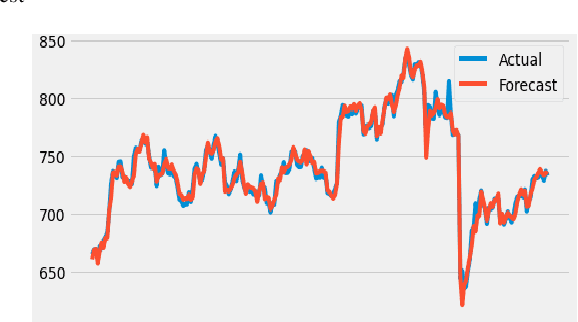

Stock Price Prediction Using Time Series, Econometric, Machine Learning, and Deep Learning Models

Nov 01, 2021

For a long-time, researchers have been developing a reliable and accurate predictive model for stock price prediction. According to the literature, if predictive models are correctly designed and refined, they can painstakingly and faithfully estimate future stock values. This paper demonstrates a set of time series, econometric, and various learning-based models for stock price prediction. The data of Infosys, ICICI, and SUN PHARMA from the period of January 2004 to December 2019 was used here for training and testing the models to know which model performs best in which sector. One time series model (Holt-Winters Exponential Smoothing), one econometric model (ARIMA), two machine Learning models (Random Forest and MARS), and two deep learning-based models (simple RNN and LSTM) have been included in this paper. MARS has been proved to be the best performing machine learning model, while LSTM has proved to be the best performing deep learning model. But overall, for all three sectors - IT (on Infosys data), Banking (on ICICI data), and Health (on SUN PHARMA data), MARS has proved to be the best performing model in sales forecasting.