Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to Edge"Time": models, code, and papers

Bilinear Input Normalization for Neural Networks in Financial Forecasting

Sep 01, 2021

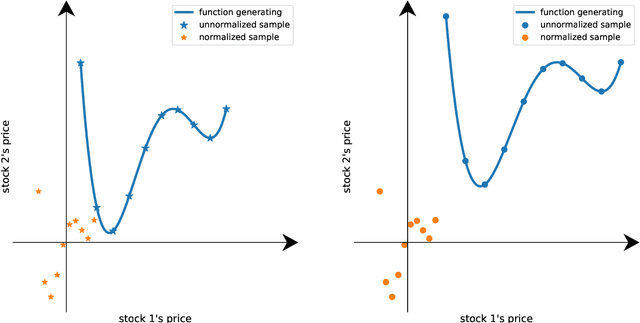

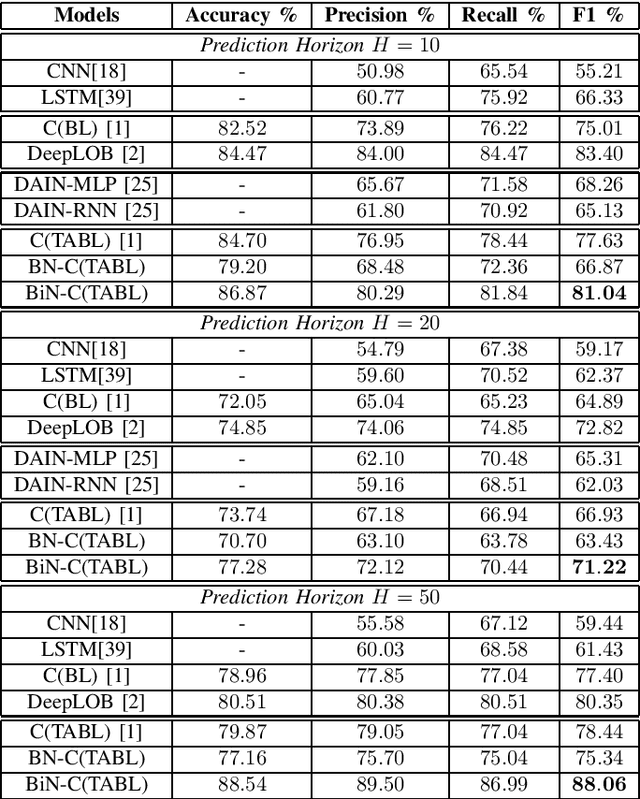

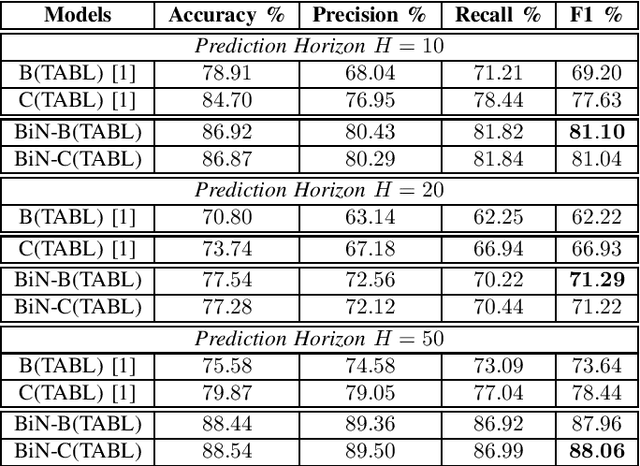

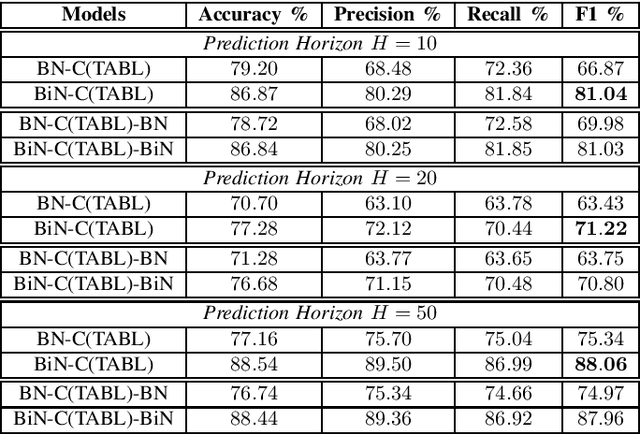

Data normalization is one of the most important preprocessing steps when building a machine learning model, especially when the model of interest is a deep neural network. This is because deep neural network optimized with stochastic gradient descent is sensitive to the input variable range and prone to numerical issues. Different than other types of signals, financial time-series often exhibit unique characteristics such as high volatility, non-stationarity and multi-modality that make them challenging to work with, often requiring expert domain knowledge for devising a suitable processing pipeline. In this paper, we propose a novel data-driven normalization method for deep neural networks that handle high-frequency financial time-series. The proposed normalization scheme, which takes into account the bimodal characteristic of financial multivariate time-series, requires no expert knowledge to preprocess a financial time-series since this step is formulated as part of the end-to-end optimization process. Our experiments, conducted with state-of-the-arts neural networks and high-frequency data from two large-scale limit order books coming from the Nordic and US markets, show significant improvements over other normalization techniques in forecasting future stock price dynamics.

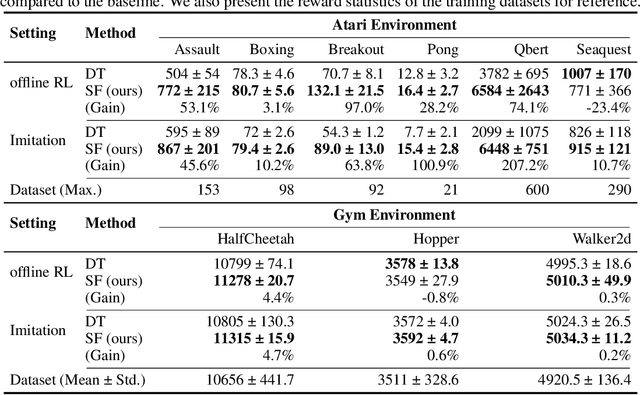

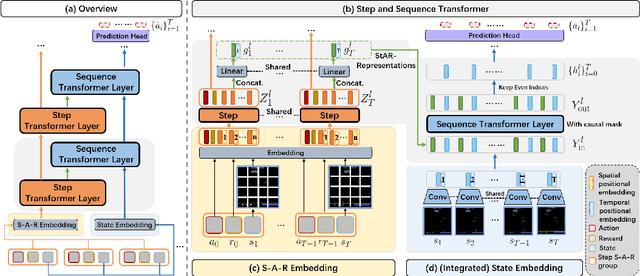

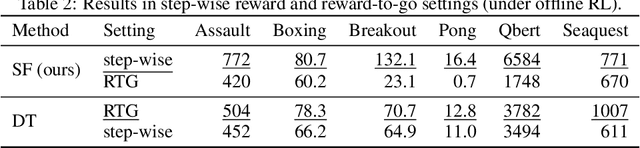

StARformer: Transformer with State-Action-Reward Representations

Oct 12, 2021

Reinforcement Learning (RL) can be considered as a sequence modeling task, i.e., given a sequence of past state-action-reward experiences, a model autoregressively predicts a sequence of future actions. Recently, Transformers have been successfully adopted to model this problem. In this work, we propose State-Action-Reward Transformer (StARformer), which explicitly models local causal relations to help improve action prediction in long sequences. StARformer first extracts local representations (i.e., StAR-representations) from each group of state-action-reward tokens within a very short time span. A sequence of such local representations combined with state representations, is then used to make action predictions over a long time span. Our experiments show that StARformer outperforms the state-of-the-art Transformer-based method on Atari (image) and Gym (state vector) benchmarks, in both offline-RL and imitation learning settings. StARformer is also more compliant with longer sequences of inputs compared to the baseline. Our code is available at https://github.com/elicassion/StARformer.

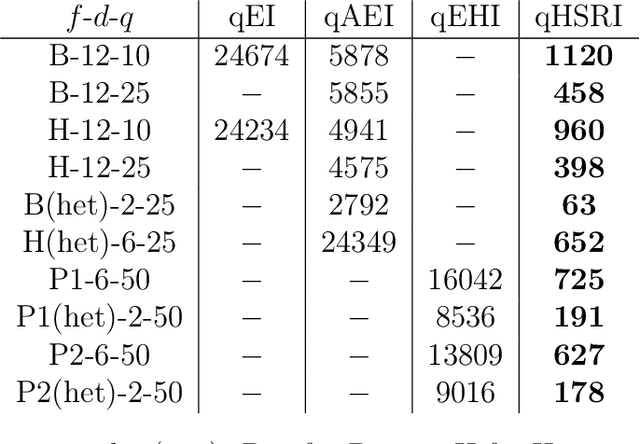

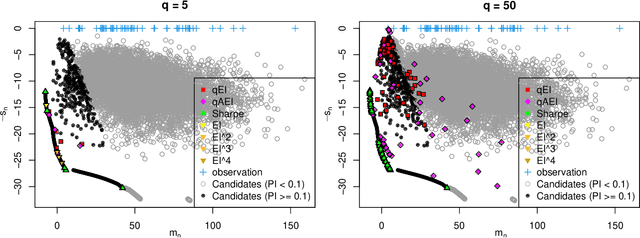

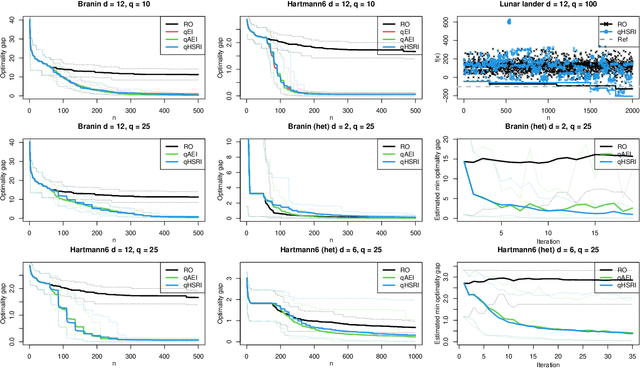

A portfolio approach to massively parallel Bayesian optimization

Oct 18, 2021

One way to reduce the time of conducting optimization studies is to evaluate designs in parallel rather than just one-at-a-time. For expensive-to-evaluate black-boxes, batch versions of Bayesian optimization have been proposed. They work by building a surrogate model of the black-box that can be used to select the designs to evaluate efficiently via an infill criterion. Still, with higher levels of parallelization becoming available, the strategies that work for a few tens of parallel evaluations become limiting, in particular due to the complexity of selecting more evaluations. It is even more crucial when the black-box is noisy, necessitating more evaluations as well as repeating experiments. Here we propose a scalable strategy that can keep up with massive batching natively, focused on the exploration/exploitation trade-off and a portfolio allocation. We compare the approach with related methods on deterministic and noisy functions, for mono and multiobjective optimization tasks. These experiments show similar or better performance than existing methods, while being orders of magnitude faster.

Robust Parameter-Free Season Length Detection in Time Series

Nov 14, 2019

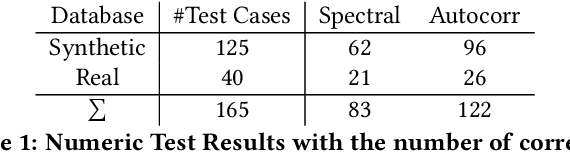

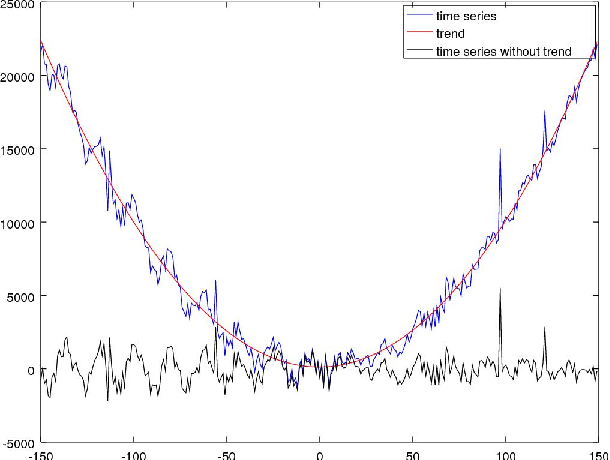

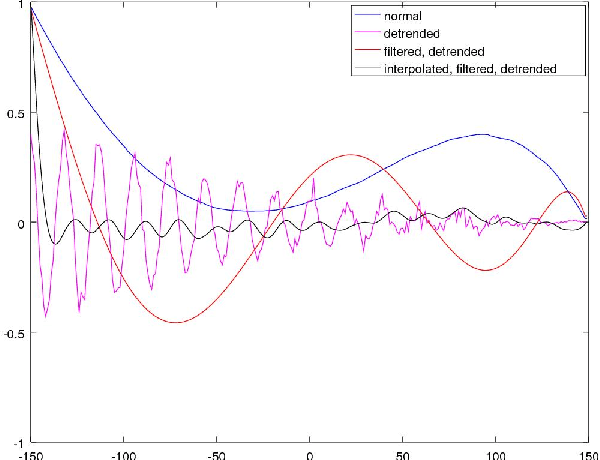

The in-depth analysis of time series has gained a lot of research interest in recent years, with the identification of periodic patterns being one important aspect. Many of the methods for identifying periodic patterns require time series' season length as input parameter. There exist only a few algorithms for automatic season length approximation. Many of these rely on simplifications such as data discretization and user defined parameters. This paper presents an algorithm for season length detection that is designed to be sufficiently reliable to be used in practical applications and does not require any input other than the time series to be analyzed. The algorithm estimates a time series' season length by interpolating, filtering and detrending the data. This is followed by analyzing the distances between zeros in the directly corresponding autocorrelation function. Our algorithm was tested against a comparable algorithm and outperformed it by passing 122 out of 165 tests, while the existing algorithm passed 83 tests. The robustness of our method can be jointly attributed to both the algorithmic approach and also to design decisions taken at the implementational level.

Neural Topic Models with Survival Supervision: Jointly Predicting Time-to-Event Outcomes and Learning How Clinical Features Relate

Jul 15, 2020

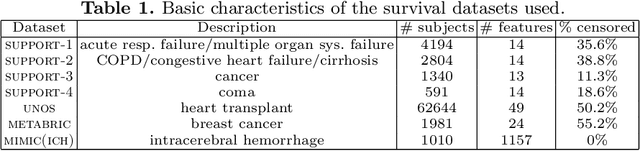

In time-to-event prediction problems, a standard approach to estimating an interpretable model is to use Cox proportional hazards, where features are selected based on lasso regularization or stepwise regression. However, these Cox-based models do not learn how different features relate. As an alternative, we present an interpretable neural network approach to jointly learn a survival model to predict time-to-event outcomes while simultaneously learning how features relate in terms of a topic model. In particular, we model each subject as a distribution over "topics", which are learned from clinical features as to help predict a time-to-event outcome. From a technical standpoint, we extend existing neural topic modeling approaches to also minimize a survival analysis loss function. We study the effectiveness of this approach on seven healthcare datasets on predicting time until death as well as hospital ICU length of stay, where we find that neural survival-supervised topic models achieves competitive accuracy with existing approaches while yielding interpretable clinical "topics" that explain feature relationships.

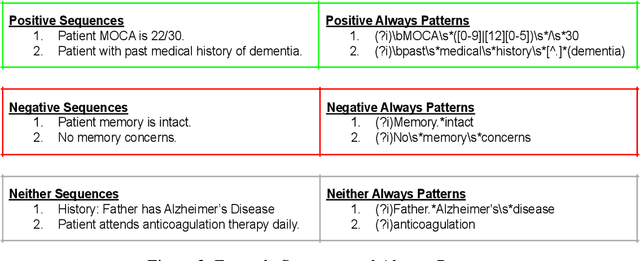

NeuraHealthNLP: An Automated Screening Pipeline to Detect Undiagnosed Cognitive Impairment in Electronic Health Records with Deep Learning and Natural Language Processing

Jan 12, 2022

Dementia related cognitive impairment (CI) affects over 55 million people worldwide and is growing rapidly at the rate of one new case every 3 seconds. With a recurring failure of clinical trials, early diagnosis is crucial, but 75% of dementia cases go undiagnosed globally with up to 90% in low-and-middle-income countries. Current diagnostic methods are notoriously complex, involving manual review of medical notes, numerous cognitive tests, expensive brain scans or spinal fluid tests. Information relevant to CI is often found in the electronic health records (EHRs) and can provide vital clues for early diagnosis, but a manual review by experts is tedious and error prone. This project develops a novel state-of-the-art automated screening pipeline for scalable and high-speed discovery of undetected CI in EHRs. To understand the linguistic context from complex language structures in EHR, a database of 8,656 sequences was constructed to train attention-based deep learning natural language processing model to classify sequences. A patient level prediction model based on logistic regression was developed using the sequence level classifier. The deep learning system achieved 93% accuracy and AUC = 0.98 to identify patients who had no earlier diagnosis, dementia-related diagnosis code, or dementia-related medications in their EHR. These patients would have otherwise gone undetected or detected too late. The EHR screening pipeline was deployed in NeuraHealthNLP, a web application for automated and real-time CI screening by simply uploading EHRs in a browser. NeuraHealthNLP is cheaper, faster, more accessible, and outperforms current clinical methods including text-based analytics and machine learning approaches. It makes early diagnosis viable in regions with scarce health care services but accessible internet or cellular services.

Pretraining & Reinforcement Learning: Sharpening the Axe Before Cutting the Tree

Oct 06, 2021

Pretraining is a common technique in deep learning for increasing performance and reducing training time, with promising experimental results in deep reinforcement learning (RL). However, pretraining requires a relevant dataset for training. In this work, we evaluate the effectiveness of pretraining for RL tasks, with and without distracting backgrounds, using both large, publicly available datasets with minimal relevance, as well as case-by-case generated datasets labeled via self-supervision. Results suggest filters learned during training on less relevant datasets render pretraining ineffective, while filters learned during training on the in-distribution datasets reliably reduce RL training time and improve performance after 80k RL training steps. We further investigate, given a limited number of environment steps, how to optimally divide the available steps into pretraining and RL training to maximize RL performance. Our code is available on GitHub

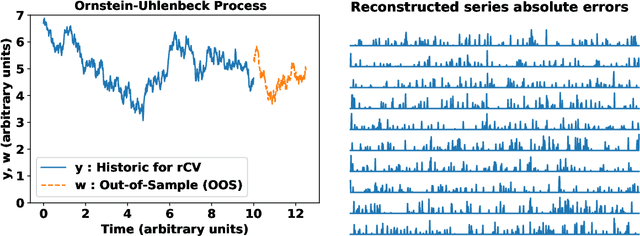

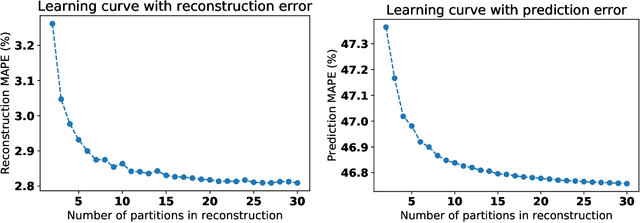

Generalised learning of time-series: Ornstein-Uhlenbeck processes

Oct 21, 2019

In machine learning, statistics, econometrics and statistical physics, $k$-fold cross-validation (CV) is used as a standard approach in quantifying the generalization performance of a statistical model. Applying this approach directly to time series models is avoided by practitioners due to intrinsic nature of serial correlations in the ordered data due to implications like absurdity of using future data to predict past and non-stationarity issues. In this work, we propose a technique called {\it reconstructive cross validation} ($rCV$) that avoids all these issues enabling generalized learning in time-series as a meta-algorithm. In $rCV$, data points in the test fold, randomly selected points from the time series, are first removed. Then, a secondary time series model or a technique is used in reconstructing the removed points from the test fold, i.e., imputation or smoothing. Thereafter, the primary model is build using new dataset coming from the secondary model or a technique. The performance of the primary model on the test set by computing the deviations from the originally removed and out-of-sample (OSS) data are evaluated simultaneously. This amounts to reconstruction and prediction errors. By this procedure serial correlations and data order is retained and $k$-fold cross-validation is reached generically. If reconstruction model uses a technique whereby the existing data points retained exactly, such as Gaussian process regression, the reconstruction itself will not result in information loss from non-reconstructed portion of the original data points. We have applied $rCV$ to estimate the general performance of the model build on simulated Ornstein-Uhlenbeck process. We have shown an approach to build a time-series learning curves utilizing $rCV$.

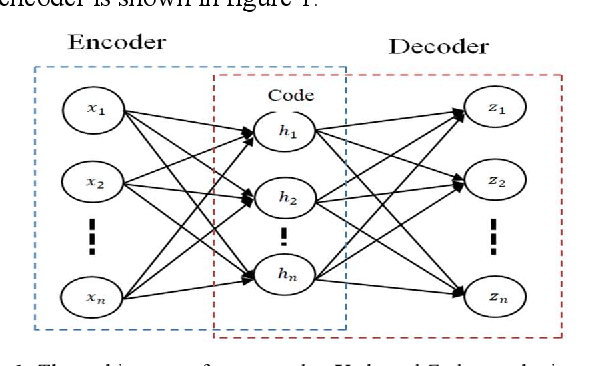

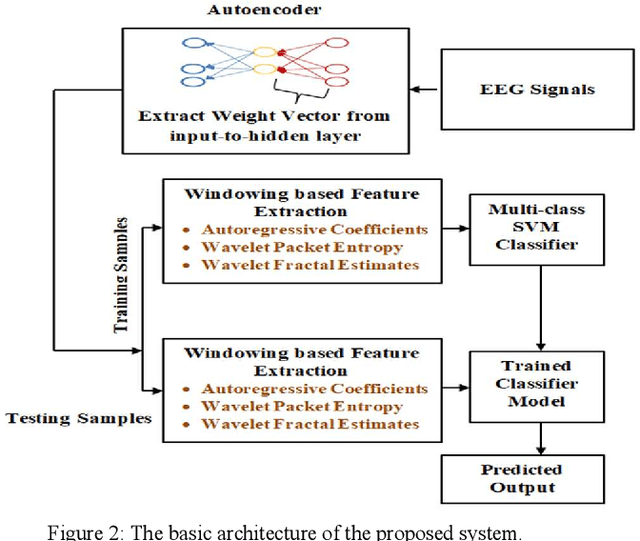

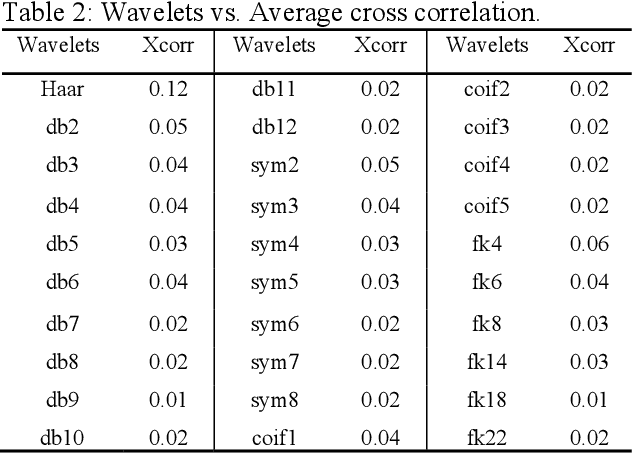

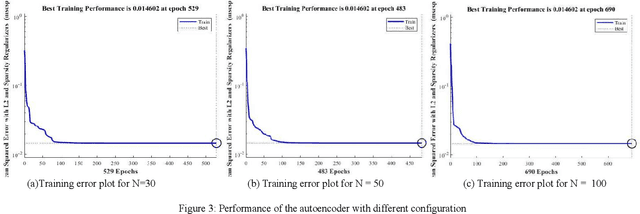

Neural Network-Based Feature Extraction for Multi-Class Motor Imagery Classification

Jan 05, 2022

Decoding of motor imagery (MI) from Electroencephalogram (EEG) is an important component of the Brain-Computer Interface (BCI) system that helps motor-disabled people interact with the outside world via external devices. The main issue in developing the EEG based BCI is the informative confusion due to the non-stationary characteristics of EEG data. In this work, an innovative idea of transforming an EEG signal into the weight vector of an unsupervised neural network called the autoencoder is proposed for the first time to solve that problem. Separate autoencoders are trained for the individual EEG data. The weight vectors are then optimized for the individual EEG signals. The EEG signals are thus represented in a new domain that is in the form of weight vectors of the individual autoencoder. The weight vectors are then used to extract features such as autoregressive coefficients (ARs), Shannon entropy (SE), and wavelet leader. A window-based feature extraction technique is implemented to capture the local features of the EEG data. Finally, extracted features are classified using a classifier network. The proposed approach is tested on two publicly accessible EEG datasets (BCI competition-III and Competition-IV) to ensure that it is as successful as and superior to the previously published methods. The proposed technique achieves a mean accuracy of 95.33 % for dataset-IIIa from BCI-III and a mean accuracy of 97% for dataset-IIa from BCI-IV for four-class EEG-based MI classification. The experimental outcomes show that the proposed approach is a promising way to increase BCI performance.

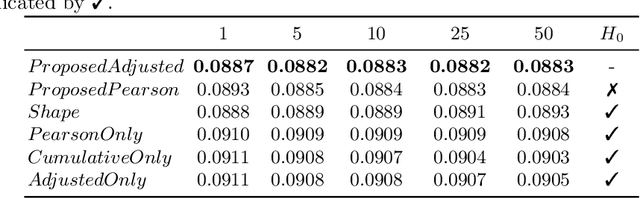

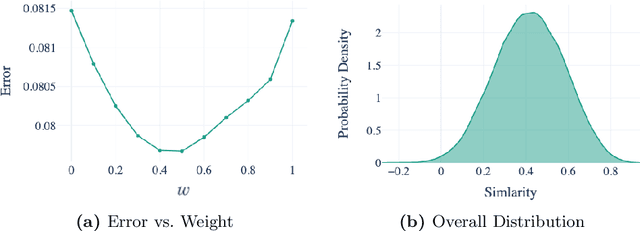

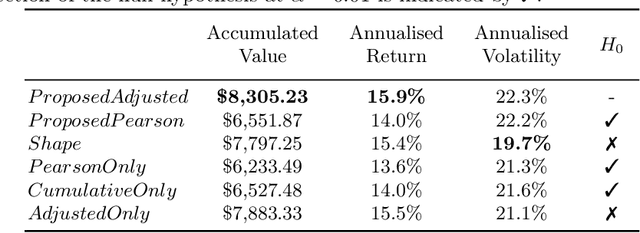

Measuring Financial Time Series Similarity With a View to Identifying Profitable Stock Market Opportunities

Jul 07, 2021

Forecasting stock returns is a challenging problem due to the highly stochastic nature of the market and the vast array of factors and events that can influence trading volume and prices. Nevertheless it has proven to be an attractive target for machine learning research because of the potential for even modest levels of prediction accuracy to deliver significant benefits. In this paper, we describe a case-based reasoning approach to predicting stock market returns using only historical pricing data. We argue that one of the impediments for case-based stock prediction has been the lack of a suitable similarity metric when it comes to identifying similar pricing histories as the basis for a future prediction -- traditional Euclidean and correlation based approaches are not effective for a variety of reasons -- and in this regard, a key contribution of this work is the development of a novel similarity metric for comparing historical pricing data. We demonstrate the benefits of this metric and the case-based approach in a real-world application in comparison to a variety of conventional benchmarks.