Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeOptimal Latent Space Forecasting for Large Collections of Short Time Series Using Temporal Matrix Factorization

Paper and Code

Dec 15, 2021

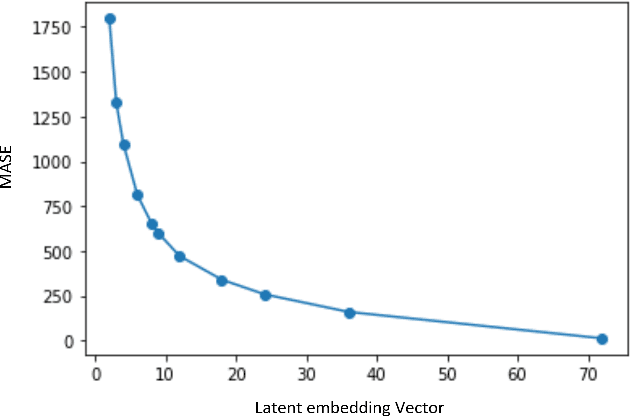

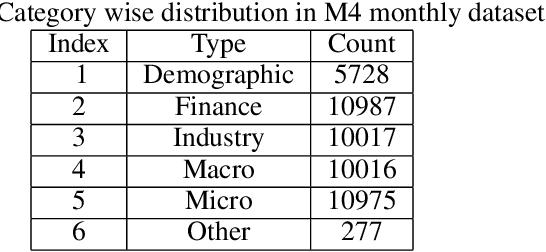

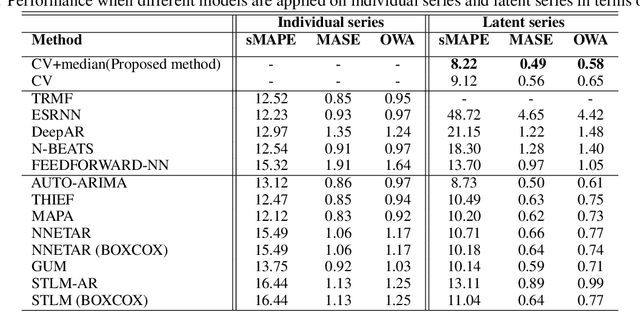

In the context of time series forecasting, it is a common practice to evaluate multiple methods and choose one of these methods or an ensemble for producing the best forecasts. However, choosing among different ensembles over multiple methods remains a challenging task that undergoes a combinatorial explosion as the number of methods increases. In the context of demand forecasting or revenue forecasting, this challenge is further exacerbated by a large number of time series as well as limited historical data points available due to changing business context. Although deep learning forecasting methods aim to simultaneously forecast large collections of time series, they become challenging to apply in such scenarios due to the limited history available and might not yield desirable results. We propose a framework for forecasting short high-dimensional time series data by combining low-rank temporal matrix factorization and optimal model selection on latent time series using cross-validation. We demonstrate that forecasting the latent factors leads to significant performance gains as compared to directly applying different uni-variate models on time series. Performance has been validated on a truncated version of the M4 monthly dataset which contains time series data from multiple domains showing the general applicability of the method. Moreover, it is amenable to incorporating the analyst view of the future owing to the low number of latent factors which is usually impractical when applying forecasting methods directly to high dimensional datasets.