Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeTopological regularization with information filtering networks

Paper and Code

May 10, 2020

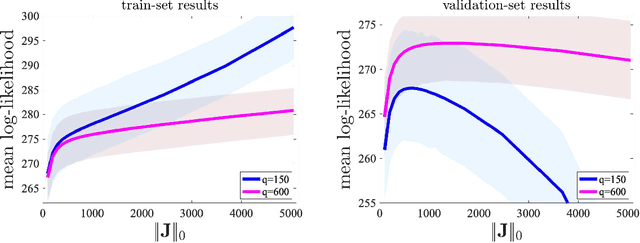

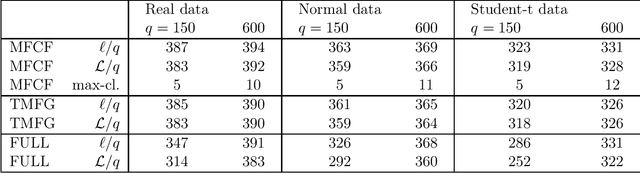

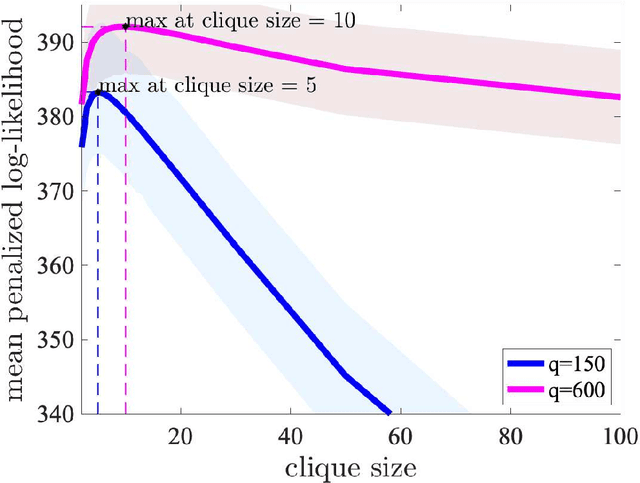

A methodology to perform topological regularization via information filtering network is introduced. This methodology can be directly applied to sparse modeling with the vast family of elliptical probability distributions. It can also be directly implemented for $L_0$ norm regularized multicollinear regression. In this paper, I describe in detail an application to sparse modeling with multivariate Student-t. A specific $L_0$ norm regularized expectation-maximization likelihood maximization procedure is proposed for this sparse Student-t case. Examples with real data from stock prices log-returns and from artificially generated data demonstrate applicability, performances, and potentials of this methodology.

* 16 pages , 2 figures, 1 table

View paper on