Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeInvestment Ranking Challenge: Identifying the best performing stocks based on their semi-annual returns

Paper and Code

Jun 20, 2019

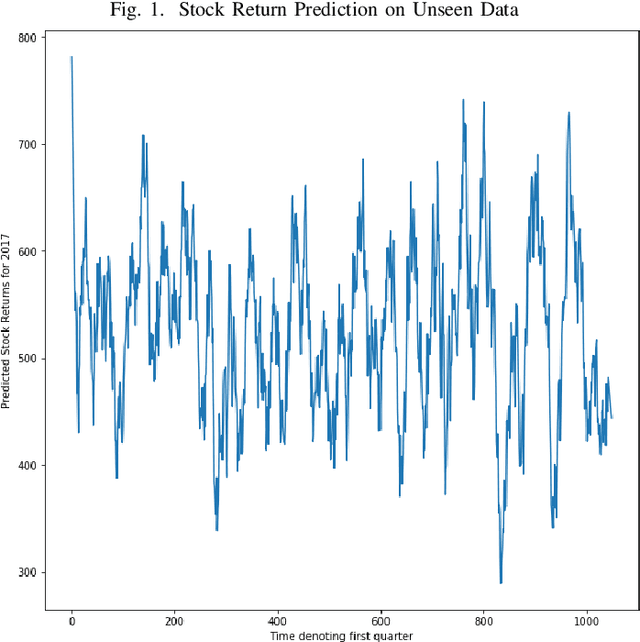

In the IEEE Investment ranking challenge 2018, participants were asked to build a model which would identify the best performing stocks based on their returns over a forward six months window. Anonymized financial predictors and semi-annual returns were provided for a group of anonymized stocks from 1996 to 2017, which were divided into 42 non-overlapping six months period. The second half of 2017 was used as an out-of-sample test of the model's performance. Metrics used were Spearman's Rank Correlation Coefficient and Normalized Discounted Cumulative Gain (NDCG) of the top 20% of a model's predicted rankings. The top six participants were invited to describe their approach. The solutions used were varied and were based on selecting a subset of data to train, combination of deep and shallow neural networks, different boosting algorithms, different models with different sets of features, linear support vector machine, combination of convoltional neural network (CNN) and Long short term memory (LSTM).