Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeNews-based forecasts of macroeconomic indicators: A semantic path model for interpretable predictions

Paper and Code

Mar 09, 2018

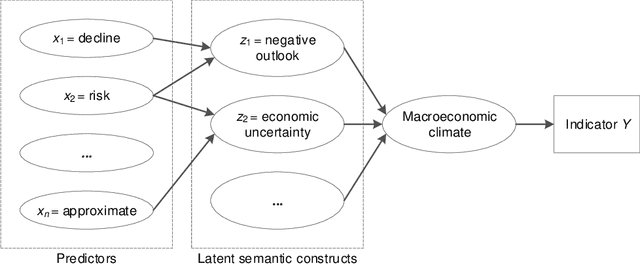

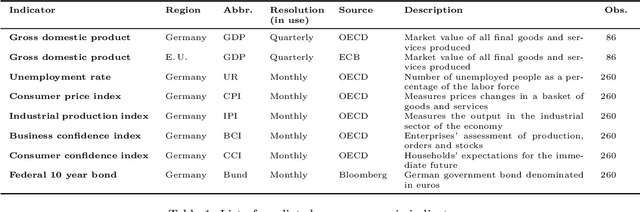

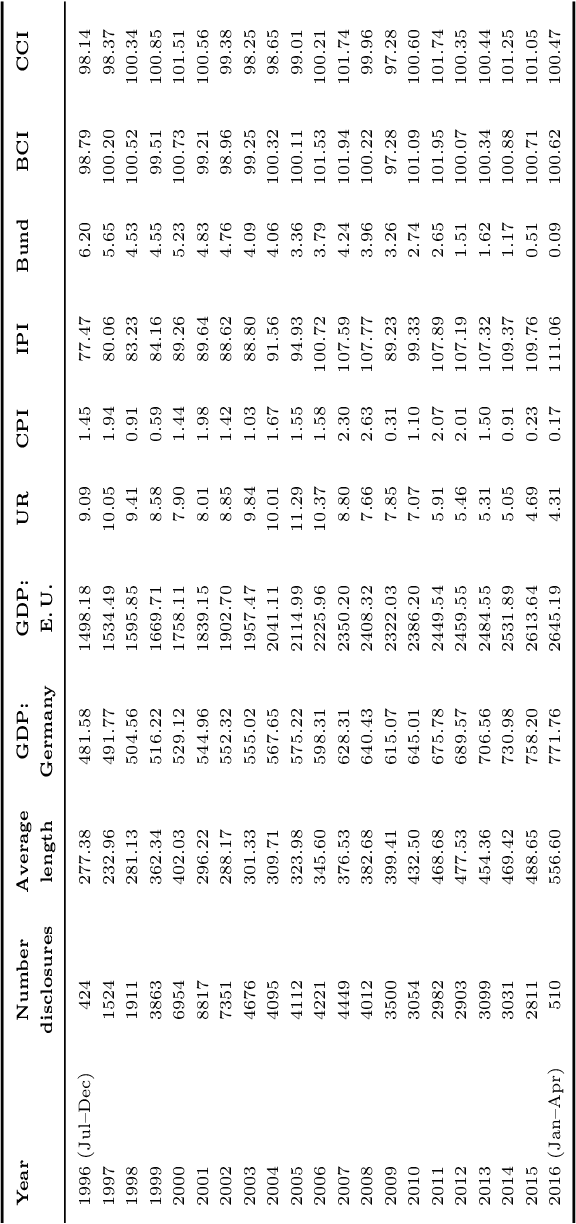

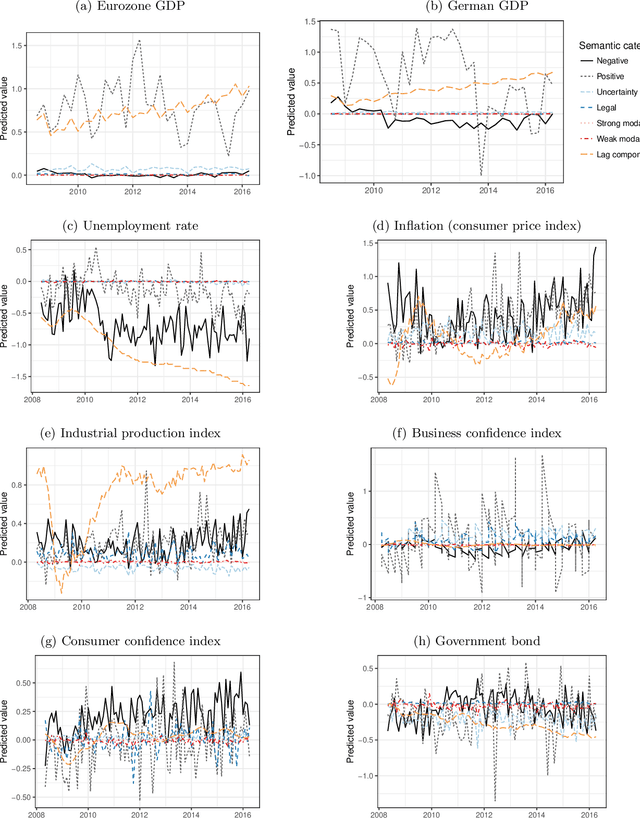

The macroeconomic climate influences operations with regard to, e.g., raw material prices, financing, supply chain utilization and demand quotas. In order to adapt to the economic environment, decision-makers across the public and private sectors require accurate forecasts of the economic outlook. Existing predictive frameworks base their forecasts primarily on time series analysis, as well as the judgments of experts. As a consequence, current approaches are often biased and prone to error. In order to reduce forecast errors, this paper presents an innovative methodology that extends lag variables with unstructured data in the form of financial news: (1) we apply a variety of models from machine learning to word counts as a high-dimensional input. However, this approach suffers from low interpretability and overfitting, motivating the following remedies. (2) We follow the intuition that the economic climate is driven by general sentiments and suggest a projection of words onto latent semantic structures as a means of feature engineering. (3) We propose a semantic path model, together with estimation technique based on regularization, in order to yield full interpretability of the forecasts. We demonstrate the predictive performance of our approach by utilizing 80,813 ad hoc announcements in order to make long-term forecasts of up to 24 months ahead regarding key macroeconomic indicators. Back-testing reveals a considerable reduction in forecast errors.