Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAaron Roth

Differentially Private Query Release Through Adaptive Projection

Mar 11, 2021

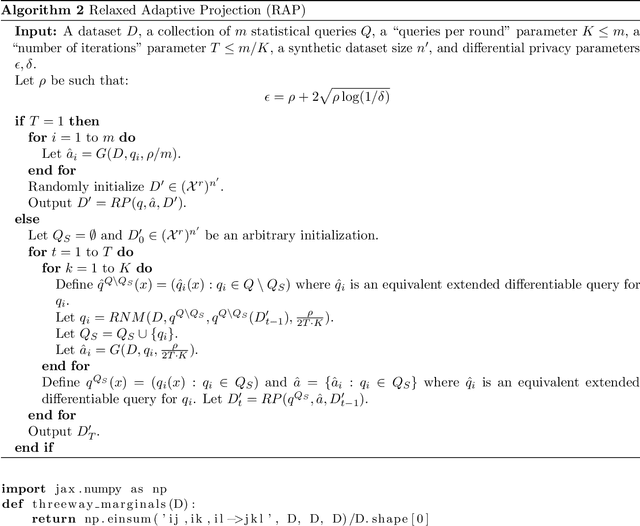

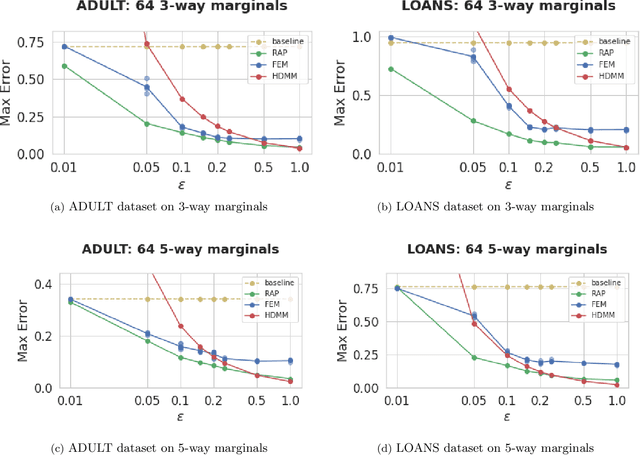

We propose, implement, and evaluate a new algorithm for releasing answers to very large numbers of statistical queries like $k$-way marginals, subject to differential privacy. Our algorithm makes adaptive use of a continuous relaxation of the Projection Mechanism, which answers queries on the private dataset using simple perturbation, and then attempts to find the synthetic dataset that most closely matches the noisy answers. We use a continuous relaxation of the synthetic dataset domain which makes the projection loss differentiable, and allows us to use efficient ML optimization techniques and tooling. Rather than answering all queries up front, we make judicious use of our privacy budget by iteratively and adaptively finding queries for which our (relaxed) synthetic data has high error, and then repeating the projection. We perform extensive experimental evaluations across a range of parameters and datasets, and find that our method outperforms existing algorithms in many cases, especially when the privacy budget is small or the query class is large.

Lexicographically Fair Learning: Algorithms and Generalization

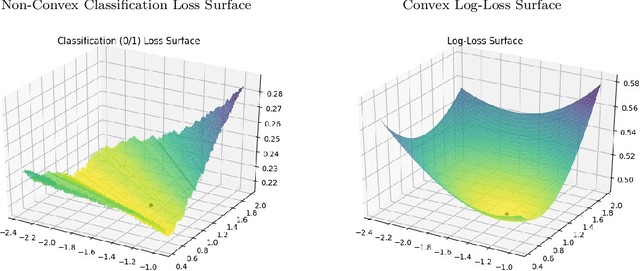

Feb 16, 2021We extend the notion of minimax fairness in supervised learning problems to its natural conclusion: lexicographic minimax fairness (or lexifairness for short). Informally, given a collection of demographic groups of interest, minimax fairness asks that the error of the group with the highest error be minimized. Lexifairness goes further and asks that amongst all minimax fair solutions, the error of the group with the second highest error should be minimized, and amongst all of those solutions, the error of the group with the third highest error should be minimized, and so on. Despite its naturalness, correctly defining lexifairness is considerably more subtle than minimax fairness, because of inherent sensitivity to approximation error. We give a notion of approximate lexifairness that avoids this issue, and then derive oracle-efficient algorithms for finding approximately lexifair solutions in a very general setting. When the underlying empirical risk minimization problem absent fairness constraints is convex (as it is, for example, with linear and logistic regression), our algorithms are provably efficient even in the worst case. Finally, we show generalization bounds -- approximate lexifairness on the training sample implies approximate lexifairness on the true distribution with high probability. Our ability to prove generalization bounds depends on our choosing definitions that avoid the instability of naive definitions.

Online Multivalid Learning: Means, Moments, and Prediction Intervals

Jan 05, 2021

We present a general, efficient technique for providing contextual predictions that are "multivalid" in various senses, against an online sequence of adversarially chosen examples $(x,y)$. This means that the resulting estimates correctly predict various statistics of the labels $y$ not just marginally -- as averaged over the sequence of examples -- but also conditionally on $x \in G$ for any $G$ belonging to an arbitrary intersecting collection of groups $\mathcal{G}$. We provide three instantiations of this framework. The first is mean prediction, which corresponds to an online algorithm satisfying the notion of multicalibration from Hebert-Johnson et al. The second is variance and higher moment prediction, which corresponds to an online algorithm satisfying the notion of mean-conditioned moment multicalibration from Jung et al. Finally, we define a new notion of prediction interval multivalidity, and give an algorithm for finding prediction intervals which satisfy it. Because our algorithms handle adversarially chosen examples, they can equally well be used to predict statistics of the residuals of arbitrary point prediction methods, giving rise to very general techniques for quantifying the uncertainty of predictions of black box algorithms, even in an online adversarial setting. When instantiated for prediction intervals, this solves a similar problem as conformal prediction, but in an adversarial environment and with multivalidity guarantees stronger than simple marginal coverage guarantees.

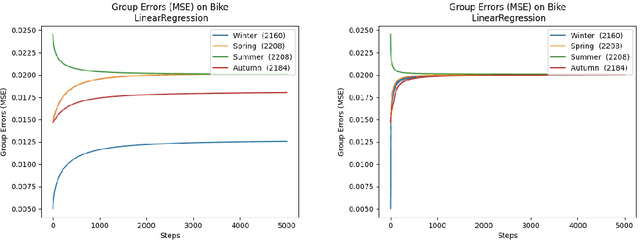

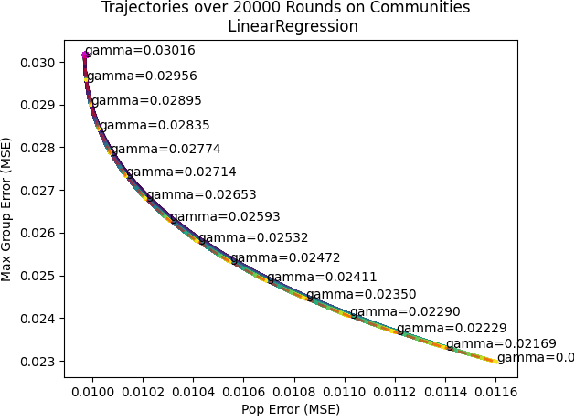

Convergent Algorithms for (Relaxed) Minimax Fairness

Nov 05, 2020

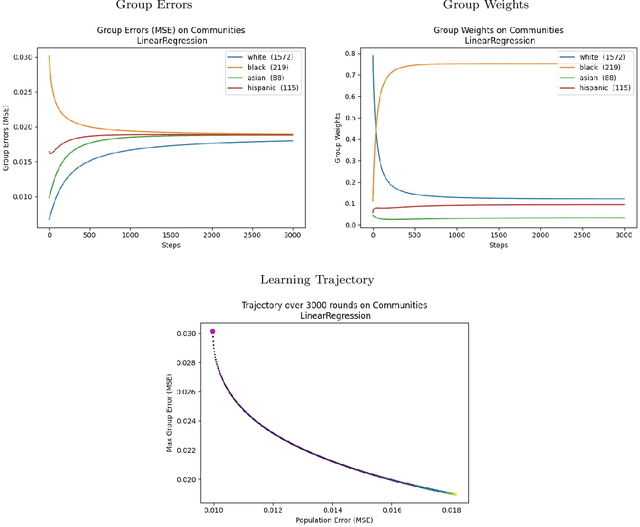

We consider a recently introduced framework in which fairness is measured by worst-case outcomes across groups, rather than by the more standard $\textit{difference}$ between group outcomes. In this framework we provide provably convergent $\textit{oracle-efficient}$ learning algorithms (or equivalently, reductions to non-fair learning) for $\textit{minimax group fairness}$. Here the goal is that of minimizing the maximum loss across all groups, rather than equalizing group losses. Our algorithms apply to both regression and classification settings and support both overall error and false positive or false negative rates as the fairness measure of interest. They also support relaxations of the fairness constraints, thus permitting study of the tradeoff between overall accuracy and minimax fairness. We compare the experimental behavior and performance of our algorithms across a variety of fairness-sensitive data sets and show cases in which minimax fairness is strictly and strongly preferable to equal outcome notions, in the sense that equal outcomes can only be obtained by artificially inflating the harm inflicted on some groups compared to what they suffer under the minimax solution.

Moment Multicalibration for Uncertainty Estimation

Aug 18, 2020We show how to achieve the notion of "multicalibration" from H\'ebert-Johnson et al. [2018] not just for means, but also for variances and other higher moments. Informally, it means that we can find regression functions which, given a data point, can make point predictions not just for the expectation of its label, but for higher moments of its label distribution as well-and those predictions match the true distribution quantities when averaged not just over the population as a whole, but also when averaged over an enormous number of finely defined subgroups. It yields a principled way to estimate the uncertainty of predictions on many different subgroups-and to diagnose potential sources of unfairness in the predictive power of features across subgroups. As an application, we show that our moment estimates can be used to derive marginal prediction intervals that are simultaneously valid as averaged over all of the (sufficiently large) subgroups for which moment multicalibration has been obtained.

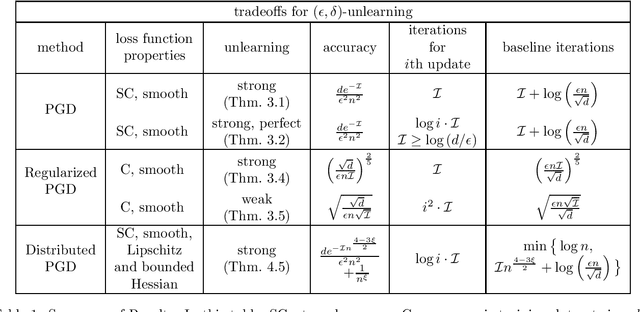

Descent-to-Delete: Gradient-Based Methods for Machine Unlearning

Jul 06, 2020

We study the data deletion problem for convex models. By leveraging techniques from convex optimization and reservoir sampling, we give the first data deletion algorithms that are able to handle an arbitrarily long sequence of adversarial updates while promising both per-deletion run-time and steady-state error that do not grow with the length of the update sequence. We also introduce several new conceptual distinctions: for example, we can ask that after a deletion, the entire state maintained by the optimization algorithm is statistically indistinguishable from the state that would have resulted had we retrained, or we can ask for the weaker condition that only the observable output is statistically indistinguishable from the observable output that would have resulted from retraining. We are able to give more efficient deletion algorithms under this weaker deletion criterion.

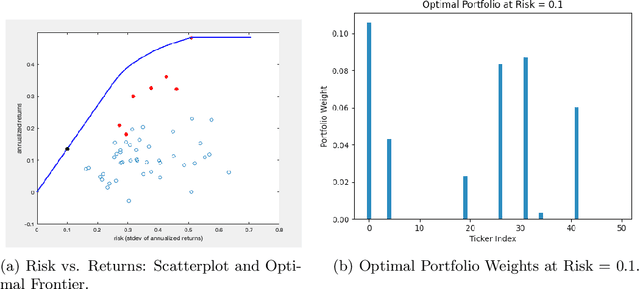

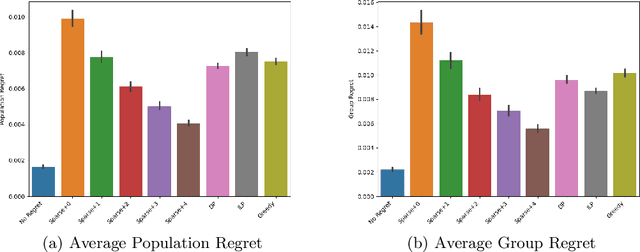

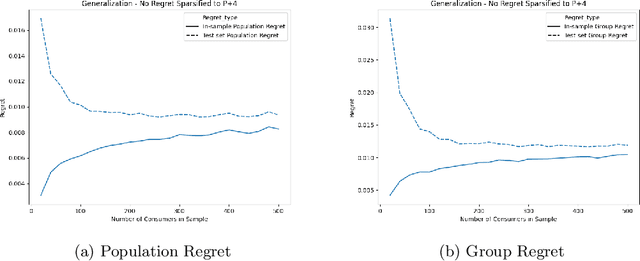

Algorithms and Learning for Fair Portfolio Design

Jun 12, 2020

We consider a variation on the classical finance problem of optimal portfolio design. In our setting, a large population of consumers is drawn from some distribution over risk tolerances, and each consumer must be assigned to a portfolio of lower risk than her tolerance. The consumers may also belong to underlying groups (for instance, of demographic properties or wealth), and the goal is to design a small number of portfolios that are fair across groups in a particular and natural technical sense. Our main results are algorithms for optimal and near-optimal portfolio design for both social welfare and fairness objectives, both with and without assumptions on the underlying group structure. We describe an efficient algorithm based on an internal two-player zero-sum game that learns near-optimal fair portfolios ex ante and show experimentally that it can be used to obtain a small set of fair portfolios ex post as well. For the special but natural case in which group structure coincides with risk tolerances (which models the reality that wealthy consumers generally tolerate greater risk), we give an efficient and optimal fair algorithm. We also provide generalization guarantees for the underlying risk distribution that has no dependence on the number of portfolios and illustrate the theory with simulation results.

Fair Prediction with Endogenous Behavior

Feb 18, 2020

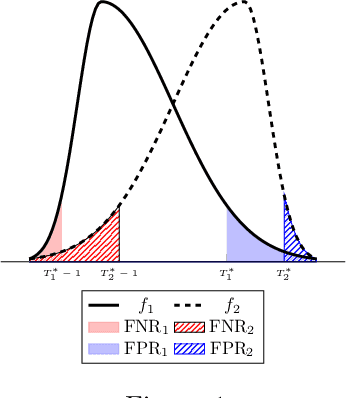

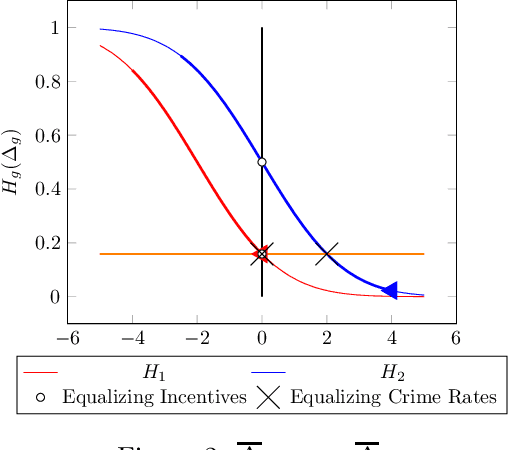

There is increasing regulatory interest in whether machine learning algorithms deployed in consequential domains (e.g. in criminal justice) treat different demographic groups "fairly." However, there are several proposed notions of fairness, typically mutually incompatible. Using criminal justice as an example, we study a model in which society chooses an incarceration rule. Agents of different demographic groups differ in their outside options (e.g. opportunity for legal employment) and decide whether to commit crimes. We show that equalizing type I and type II errors across groups is consistent with the goal of minimizing the overall crime rate; other popular notions of fairness are not.

Pipeline Interventions

Feb 16, 2020

We introduce the \emph{pipeline intervention} problem, defined by a layered directed acyclic graph and a set of stochastic matrices governing transitions between successive layers. The graph is a stylized model for how people from different populations are presented opportunities, eventually leading to some reward. In our model, individuals are born into an initial position (i.e. some node in the first layer of the graph) according to a fixed probability distribution, and then stochastically progress through the graph according to the transition matrices, until they reach a node in the final layer of the graph; each node in the final layer has a \emph{reward} associated with it. The pipeline intervention problem asks how to best make costly changes to the transition matrices governing people's stochastic transitions through the graph, subject to a budget constraint. We consider two objectives: social welfare maximization, and a fairness-motivated maximin objective that seeks to maximize the value to the population (starting node) with the \emph{least} expected value. We consider two variants of the maximin objective that turn out to be distinct, depending on whether we demand a deterministic solution or allow randomization. For each objective, we give an efficient approximation algorithm (an additive FPTAS) for constant width networks. We also tightly characterize the "price of fairness" in our setting: the ratio between the highest achievable social welfare and the highest social welfare consistent with a maximin optimal solution. Finally we show that for polynomial width networks, even approximating the maximin objective to any constant factor is NP hard, even for networks with constant depth. This shows that the restriction on the width in our positive results is essential.

Optimal, Truthful, and Private Securities Lending

Dec 12, 2019We consider a fundamental dynamic allocation problem motivated by the problem of $\textit{securities lending}$ in financial markets, the mechanism underlying the short selling of stocks. A lender would like to distribute a finite number of identical copies of some scarce resource to $n$ clients, each of whom has a private demand that is unknown to the lender. The lender would like to maximize the usage of the resource $\mbox{---}$ avoiding allocating more to a client than her true demand $\mbox{---}$ but is constrained to sell the resource at a pre-specified price per unit, and thus cannot use prices to incentivize truthful reporting. We first show that the Bayesian optimal algorithm for the one-shot problem $\mbox{---}$ which maximizes the resource's expected usage according to the posterior expectation of demand, given reports $\mbox{---}$ actually incentivizes truthful reporting as a dominant strategy. Because true demands in the securities lending problem are often sensitive information that the client would like to hide from competitors, we then consider the problem under the additional desideratum of (joint) differential privacy. We give an algorithm, based on simple dynamics for computing market equilibria, that is simultaneously private, approximately optimal, and approximately dominant-strategy truthful. Finally, we leverage this private algorithm to construct an approximately truthful, optimal mechanism for the extensive form multi-round auction where the lender does not have access to the true joint distributions between clients' requests and demands.